RinggitPlus Credit Card Latest Promotions 2026

Credit card sign-up offers in Malaysia include brand new Apple products (latest iPhones, MacBooks, iPads, or Apple Watches), Touch 'n Go credits, and cash vouchers. When you apply through RinggitPlus, you get exclusive access to promotions with higher-value gifts than what's available elsewhere. These promotions change regularly throughout the year, with new offers typically launching on Mondays.

RinggitPlus compares live sign-up offers from all major banks so you can find the best gift for your situation. Whether you want cashback, rewards, air miles, or premium gadgets, we help you choose a card that matches your spending habits.

New promotions typically launch on Mondays, with occasional flash deals announced mid-week. Bookmark this page and check back regularly to see the latest gifts before they expire.

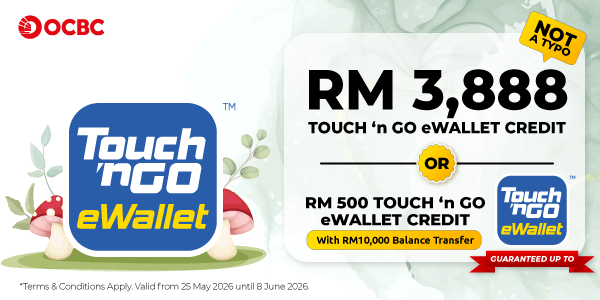

OCBC Credit Cards Promotion

| Sign Up Gift |

RM3,888 Touch 'n Go E-Wallet Credit (For every 38th qualified applicant based on the Approval List from the Bank, with or without Balance Transfer, capped at 3 units) RM500 Touch 'n Go E-Wallet Credit (Guaranteed to qualified applicants who successfully get approval and maintain a Balance Transfer of RM10,000 or more using the Eligible Card) RM400 Touch 'n Go E-Wallet Credit (Guaranteed to qualified applicants who successfully get approval and maintain a Balance Transfer of less than RM10,000 using the Eligible Card) RM300 Touch 'n Go E-Wallet Credit (Guaranteed to qualified applicants who are not awarded the Premium Gift, Primary Guaranteed Gift, or Secondary Guaranteed Gift) |

| Sign Up Period | 25 May 2026 - 8 June 2026 |

| Requirement | Apply, get approved by OCBC, activate the new card, and subsequently spend a minimum of RM100 in retail transactions within 60 days of the card approval date. |

| Eligible Card |

OCBC Cashflo MasterCard OCBC 90⁰N Visa Card OCBC 365 MasterCard OCBC Titanium MasterCard Pink OCBC Titanium MasterCard Blue |

| Eligible Applicant |

New customers only. Existing primary cardholders, those who have had their OCBC credit card(s) application approved or denied within 12 months, and those who have cancelled their OCBC credit card(s) within 12 months before the date of the flash deal application, are not eligible. Terms and conditions apply. |

HSBC Credit Cards Promotion

| Sign Up Gift |

Apple iPad Pro M5 with Apple Pencil Pro (For every 38th qualified applicant based on the Approval List by the Bank, capped at 2 units)

RM500 Touch 'n Go E-Wallet Credit (Guaranteed to qualified applicants who are not selected to receive the premium gift above) |

| Sign Up Period | 20 May 2026 - 3 June 2026 |

| Requirement |

Apply, get approved by HSBC, activate the new card, and subsequently spend a minimum of RM3,000 in retail transactions within 60 days of the card approval date.

|

| Eligible Card |

HSBC Visa Signature Credit Card

HSBC TravelOne Credit Card HSBC Live+ Credit Card |

| Eligible Applicant |

New customers only.

Existing primary cardholders, those who have had their HSBC credit card(s) application approved or denied within 12 months, and those who have cancelled their HSBC credit card(s) within 12 months before the date of the flash deal application, are not eligible. Terms and conditions apply. |

UOB Credit Cards Promotion

| Sign Up Gift |

RM200 Touch 'n Go E-Wallet Credit (Guaranteed to qualified applicants who have applied for UOB Visa Infinite Card, UOB PRVI Miles Elite Card, UOB World Card, UOB Lady’s Solitaire Card, and UOB Platinum Business Card)

RM100 Touch 'n Go E-Wallet Credit (Guaranteed to qualified applicants who have applied for UOB Preferred Card, UOB Lady’s Card, UOB ONE Card, UOB EVOL Card, Lazada UOB Card, and UOB Simple Card) |

| Sign Up Period | 4 May 2026 - 3 June 2026 |

| Requirement |

For UOB Visa Infinite Card, UOB PRVI Miles Elite Card, UOB World Card, UOB Lady’s Solitaire Card, and UOB Platinum Business Card Apply with RinggitPlus, get approved by the bank, activate the card, and make a minimum amount of RM400 in retail transactions (“Retail Spend”) within sixty (60) calendar days from the Credit Card approval date to be eligible. For UOB Preferred Card, UOB Lady’s Card, UOB ONE Card, UOB EVOL Card, Lazada UOB Card, and UOB Simple Card Apply with RinggitPlus, get approved by the bank, activate the card, and make a minimum amount of RM200 in retail transactions (“Retail Spend”) within sixty (60) calendar days from the Credit Card approval date to be eligible. |

| Eligible Card |

UOB Visa Infinite Card

UOB PRVI Miles Elite Card UOB World Card UOB Lady’s Solitaire Card UOB Platinum Business Card UOB Preferred Card UOB Lady’s Card UOB ONE Card UOB EVOL Card Lazada UOB Card UOB Simple Card |

| Eligible Applicant |

New customers only.

Existing primary cardholders and those who have cancelled their UOB credit card(s) within 12 months before the date of the flash deal application are not eligible. Terms and conditions apply. |

Maybank Credit Cards Promotion

| Sign Up Gift | Nintendo Switch 2 (For every 40th qualified applicant who has completed their online application within the Promotion Period, and has met the eligibility criteria, capped at 5 units) |

| Sign Up Period | 25 May 2026 - 22 June 2026 |

| Requirement |

Apply, get approved by Maybank, activate the new card, and subsequently spend a minimum of RM300 in retail transactions within 30 calendar days from the card's approval date to be eligible.

For applicants applying for the Maybank 2 Gold Cards and Maybank 2 Platinum Cards, the retail transaction must be made on the Mastercard. |

| Eligible Card |

Maybank World Elite MasterCard

Maybank Islamic MasterCard Ikhwan Platinum Card-i Maybank Islamic MasterCard Ikhwan Gold Card-i Maybank Islamic World Elite Mastercard Ikhwan Maybank Islamic myimpact Ikhwan Mastercard Platinum Credit Card-i Maybank 2 Gold Cards Maybank 2 Platinum Cards Maybank Grab Mastercard Platinum |

| Eligible Applicant |

New customers only.

Existing principal cardholders who hold any Maybank credit cards or those who have cancelled their Maybank credit card within 6 months before the date of the flash deal application are not eligible. Terms and conditions apply. |

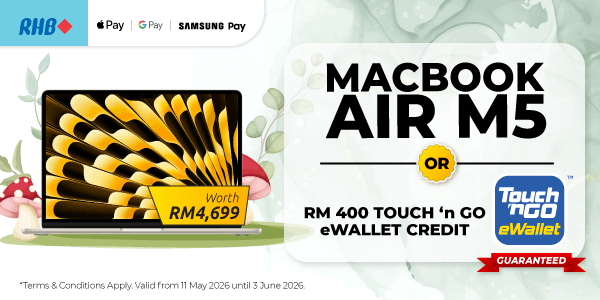

RHB Credit Cards Promotion

| Sign Up Gift |

Apple MacBook Air M5 (For one (1) qualified random winner per week based on the Approval List from the Bank, capped at 3 units)

RM400 Touch 'n Go E-Wallet Credit (Guaranteed to qualified applicants who have two (2) approved RHB credit card applications) RM200 Touch 'n Go E-Wallet Credit (Guaranteed to qualified applicants who are not selected to receive the gifts mentioned above) |

| Sign Up Period | 11 May 2026 - 3 June 2026 |

| Requirement |

For applicants who apply for one (1) RHB Credit Card Get approved, activate your new RHB credit card, and subsequently make one (1) retail transaction with no minimum purchase amount as a Principal cardholder, within 60 days of the card's approval date. For applicants who apply for two (2) RHB Credit Cards Get approved, activate your new RHB credit cards, and subsequently make one (1) retail transaction on BOTH the cards with no minimum purchase amount as a Principal cardholder, within 60 days of the card's approval date. |

| Eligible Card |

RHB Visa Infinite

RHB Visa Signature MyEG-RHB Credit Card RHB World MasterCard Credit Card RHB World MasterCard Credit Card-i RHB Cash Back Visa Credit Card RHB Cash Back MasterCard Credit Card RHB Islamic Cash Back Credit Card-i RHB Rewards Visa Credit Card RHB Rewards MasterCard Credit Card RHB Rewards Visa Credit Card-i RHB Shell Visa Credit Card RHB Shell Visa Credit Card-i |

| Eligible Applicant |

New customers only.

Existing principal cardholders and those who have cancelled their RHB credit card within 12 months from the date of the current application are not eligible. Terms and conditions apply. |

AmBank Credit Cards Promotion

| Sign Up Gift |

Apple Watch Series 11 (For every 38th qualified applicant who meets the requirements, and based on the Bank's approval list, capped at 4 units)

RM200 Touch 'n Go E-Wallet Credit (Guaranteed to qualified applicants who applied for the Visa Signature Card, Visa Infinite Card, Visa Infinite Card-i, Visa Signature Card-i, BonusLink Visa Signature Card, and meet the requirements, based on the Bank's approval list) RM100 Touch 'n Go E-Wallet Credit (Guaranteed to qualified applicants who applied for the Cash Rebate Visa Platinum Card, BonusLink Visa Platinum Card, Visa Platinum CARz Card-i, Visa Platinum Card, Visa Platinum Card-i, UnionPay Platinum Card and meet the requirements, based on the Bank's approval list) |

| Sign Up Period | 25 May 2026 - 22 June 2026 |

| Requirement |

For AmBank Visa Infinite Card, AmBank Islamic Visa Infinite Card-i, AmBank Visa Signature Card, AmBank Islamic Visa Signature Card-i, AmBank BonusLink Visa Signature Card Apply, get approved by the Bank and activate the card before 22 July 2026 (11:59 PM), then spend a minimum of RM400 in retail transactions within sixty (60) calendar days upon the approval date to be eligible. For AmBank Cash Rebate Visa Platinum Card, AmBank BonusLink Visa Platinum Card, AmBank Islamic Visa Platinum CARz Card-i, AmBank Visa Platinum Card, AmBank Islamic Visa Platinum Card-i, AmBank UnionPay Platinum Card Apply, get approved by the Bank and activate the card before 22 July 2026 (11:59 PM), then spend a minimum of RM200 in retail transactions within sixty (60) calendar days upon the approval date to be eligible. |

| Eligible Card |

AmBank Visa Infinite Card

AmBank Islamic Visa Infinite Card-i AmBank Visa Signature Card AmBank Islamic Visa Signature Card-i AmBank BonusLink Visa Signature Card AmBank Cash Rebate Visa Platinum Card AmBank BonusLink Visa Platinum Card AmBank Islamic Visa Platinum CARz Card-i AmBank Visa Platinum Card AmBank Islamic Visa Platinum Card-i AmBank UnionPay Platinum Card |

| Eligible Applicant |

New customers only.

Existing primary cardholders of an AmBank Credit Card and those who have cancelled any of their credit cards issued by the Bank in the last 12 months from the date of application are not eligible. Terms and conditions apply. |

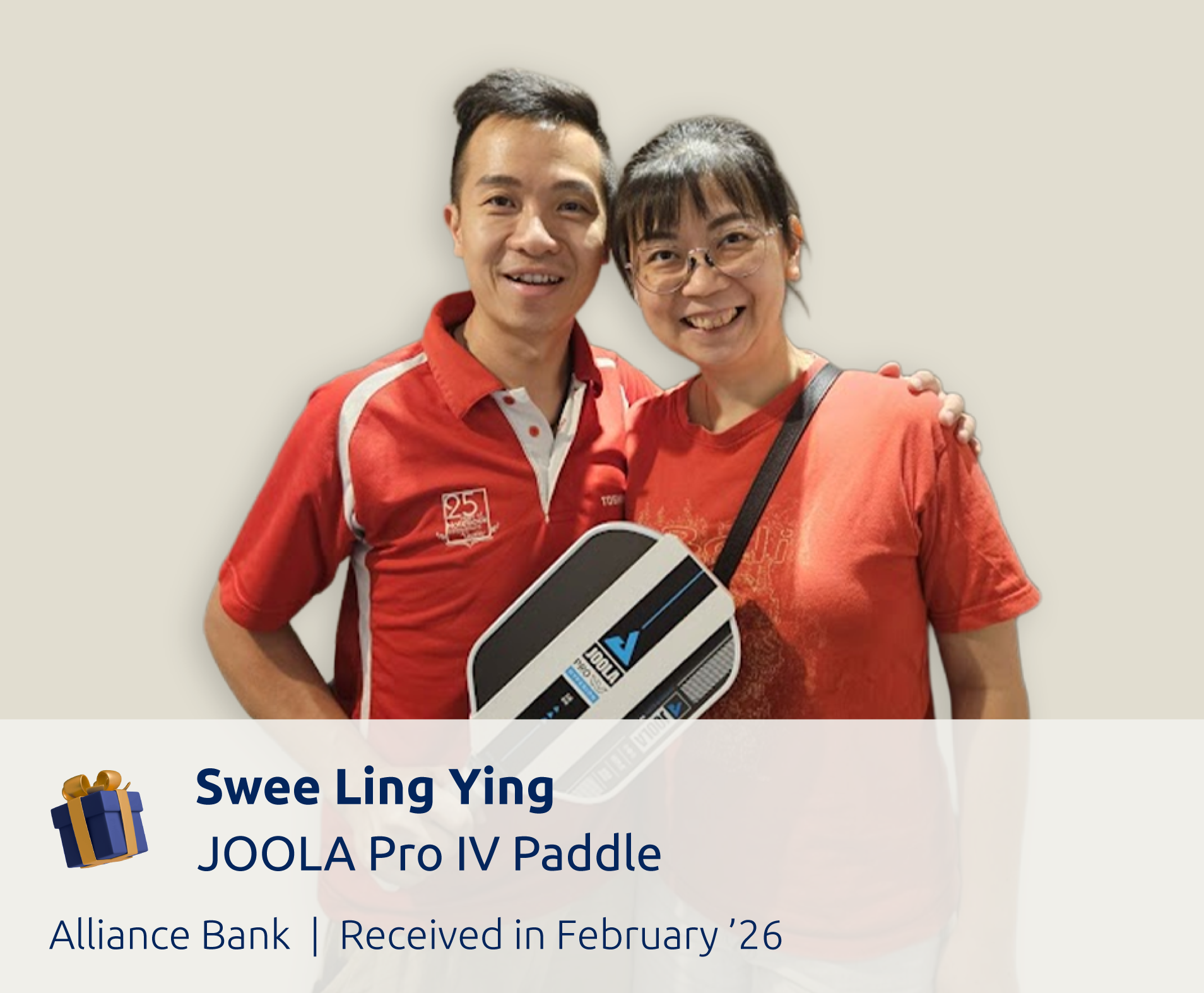

Alliance Bank Credit Cards Promotion

| Sign Up Gift |

Meet the qualifying requirement to earn campaign entries and receive Blind Box rewards, such as: Apple iPhone 17 Apple Watch Series 11 Apple AirPods 4 Cashback Up To RM17 |

| Sign Up Period | 4 May 2026 - 30 June 2026 |

| Requirement |

Apply, get approved by Alliance Bank by 15 August 2026, activate the card, and spend a minimum of RM400 in retail transactions in a single receipt within the campaign period to earn campaign entries.

|

| Eligible Card |

Alliance Bank Visa Platinum Credit Card

Alliance Bank Visa Infinite Credit Card Alliance Bank Visa Virtual Credit Card |

| Eligible Applicant |

New customers only.

Existing principal cardholders of Alliance Bank Visa or Mastercard Credit Card, and individuals who have closed or cancelled any of their credit cards with the bank in the last 7 years from the date of application are not eligible. Terms and conditions apply. |

Frequently Asked Questions

These FAQs explain how credit card approvals and sign-up gift redemptions work on RinggitPlus. If your question is related to bank approval status or gift delivery timelines, you will likely find the answer below.

How can I check my application status?

Banks handle approvals, not RinggitPlus. Contact your bank's credit card hotline for application status updates. The phone number is on your application confirmation email or on the bank's official website. We can't speed up the bank's decision or access their internal systems.

If your card is already approved and activated but you're waiting for your sign-up gift, email us at [email protected]. We can verify your eligibility against the bank's approval list.

I’ve received my credit card, but I’m still waiting for my reward. What should I do?

Please wait up to 60 days from your card approval date, or from the date you completed the RinggitPlus Rewards Redemption Form (whichever is later), to receive your gift redemption email or reward.

If you have not completed the Rewards Redemption Form yet, check your inbox and spam folder for the redemption email from RinggitPlus. Completing the form promptly helps avoid delays in the gift delivery process. If it has been more than 60 days, or you are facing issues completing the form, email us at [email protected], and we will assist you.

What is a unique ID, and why is it important?

Your unique ID is a reference code that links your credit card application to your sign-up gift. Think of it as a tracking number.

You'll find this ID in the gift redemption email from RinggitPlus. Use it when completing the Rewards Redemption Form. An incorrect ID delays processing because we can't match your details to the bank's approval list.

If you can't find your unique ID or didn't receive the redemption email, email [email protected].

I can’t remember if I’ve completed my Rewards Redemption Form. What should I do?

Click the redemption link in the RinggitPlus email you received.

If you've already submitted the form, you'll see confirmation. If the form opens blank, you haven't submitted it yet. Check both your main inbox and spam folder for the email.

Need confirmation that we received your submission? Email [email protected] with your name and unique ID.

I’ve completed my Rewards Redemption Form. When will I receive my reward?

Delivery times vary by gift type:

- Physical gifts (iPhone, iPad, MacBook, Apple Watch): 21-28 working days after completing the redemption form

- E-wallet credits (Touch 'n Go): Up to 60 days after bank verification

- Cash transfers (DuitNow): Up to 60 days after bank verification

Stock availability may extend physical gift delivery. If it's been longer than 28 working days, email [email protected] with your unique ID.

How do I modify my delivery address after completing the Rewards Redemption Form?

Contact us at [email protected] immediately with your unique ID and updated address.

Address changes are only possible if your gift hasn't been shipped yet. Once dispatched, coordinate with the courier or collect from the original address.

What counts as retail spending?

Retail spending includes: groceries, dining, petrol, online shopping, utilities, e-wallet top-ups (Touch 'n Go, Boost, BigPay), standing instructions, auto-billing, and insurance/takaful payments.

Does NOT count: Cash advances, balance transfers, Easy Payment Plan (EPP) conversions, interest charges, annual fees, government payments (LHDN, JPJ), or charity payments.

Definitions vary by bank, so always check the promotion's terms and conditions.

Can I change my gift?

No. Gifts cannot be changed or exchanged.

The gift offered is fixed by the promotion period during which you applied. If the promotion offers an iPhone, you can't request a MacBook instead. For lucky draw promotions ("every 38th applicant" wins premium gifts), non-winners receive the guaranteed secondary gift instead.

Why was I not selected as a winner for a flash deal?

Flash deals have strict eligibility criteria. Common reasons for non-selection:

- You didn't meet the minimum spending requirement

- Your application was approved outside the campaign period

- You're not a new customer (currently hold or recently cancelled a card from that bank)

- You weren't selected in the lucky draw (odds: typically 1 in 38 to 40, so 2.5% to 2.6% chance)

Check the winners' list to confirm your status. If you weren't selected as a premium winner, you may still qualify for the guaranteed secondary gift if all other conditions are met.

10. Does RinggitPlus collect any of my data during the application process?

Yes, but only limited information: name, email address, credit card product applied for, application reference number, and application date.

This information is used only to verify your gift eligibility against the bank's approval list. We don't collect sensitive details like IC number, income, bank statements, or employment information (banks collect those directly).

All data is protected under Malaysia's Personal Data Protection Act (PDPA) and is not shared with third parties. See our Privacy Policy and Notice for details.

Still Have Questions?

For additional help with DuitNow transfers, warranty information, redemption timelines, and troubleshooting, refer to our detailed FAQ article.

Contact us directly: Email: [email protected]