What You Need To Know About The New Regulations On Investment-Linked Insurance

Jacie Tan

21st June 2019 - 4 min read

If you have or are planning to purchase an investment-linked product (ILP) insurance policy, then you should take note of the new regulations by Bank Negara that will come into effect from 1 July 2019. In January, Bank Negara released a policy document that set several new requirements that investment-linked insurance providers must adhere to from 1 July 2019 onwards. These requirements were designed with the primary objective of protecting the interests of consumers.

According to the Bank Negara policy document on investment-linked businesses, insurance providers must adhere to three main requirements:

- Implementation of standards on Minimum Allocation Rates to protect the account values of investment-linked policy/certificate owners;

- Minimum standards on sustainability tests and communication to policy/certificate owners to improve long term persistency of IL policies/certificates and consumer awareness; and

- Strengthened disclosure standards on product illustration to facilitate more informed decision-making by consumers.

As you can see, these requirements are quite broad in nature and rather complicated to understand, so here are some of the specific changes that you will be seeing in ILP policies from 1 July onwards.

The minimum allocation rate (MAR) must be set to at least 60%

The minimum allocation rate (MAR) refers to the minimum proportion of premiums that is allocated in the policy owner’s unit fund(s) of choice (i.e. the “investment” portion of the policy) before the deduction of any charges Effective 1 July 2019, the MAR for ILP policies longer than 20 years will be set at a MAR of at least 60% – this is being done with the intention of protecting your policy’s sustainability in the long run.

| Year of premium payment or contribution | MAR |

| 1-3 | 60% |

| 4-6 | 80% |

| 7-10 | 95% |

| 11 onwards | 100% |

You will get an annual statement detailing your expected duration of cover

From 1 January 2020, all policy owners will receive a yearly statement which contains the expected duration of their insurance cover based on their current cash values (i.e. how long can the policy run if you stopped paying premiums). So, don’t panic if you receive this annual statement for the first time next January – it is the start of a yearly occurrence that will help you be aware of how long your insurance cover is predicted to last based on your current premium and fund performance.

You will get a pre-lapse notice

For policies sold before 1 July 2019, insurance companies have an obligation to send a pre-lapse notice for ILPs that will lapse within the next 12 months.

Premiums should be sustainable for the entire contract term

For policies sold after 1 July 2019, insurers must set premiums that are expected to be sustainable until the end of the contract term. In order to set premiums sustainably, insurers must make assessments that are current, specific to the individual ILP owner, and relevant.

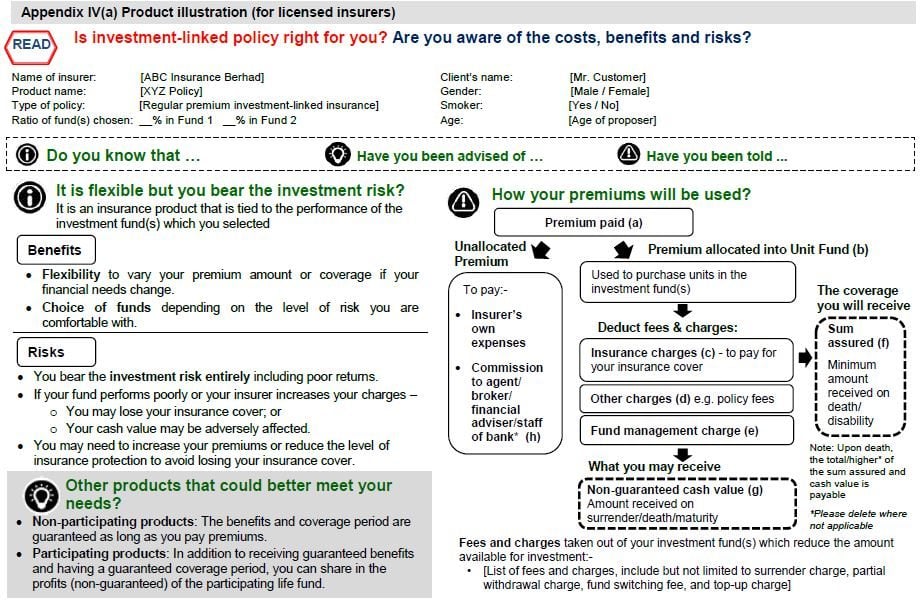

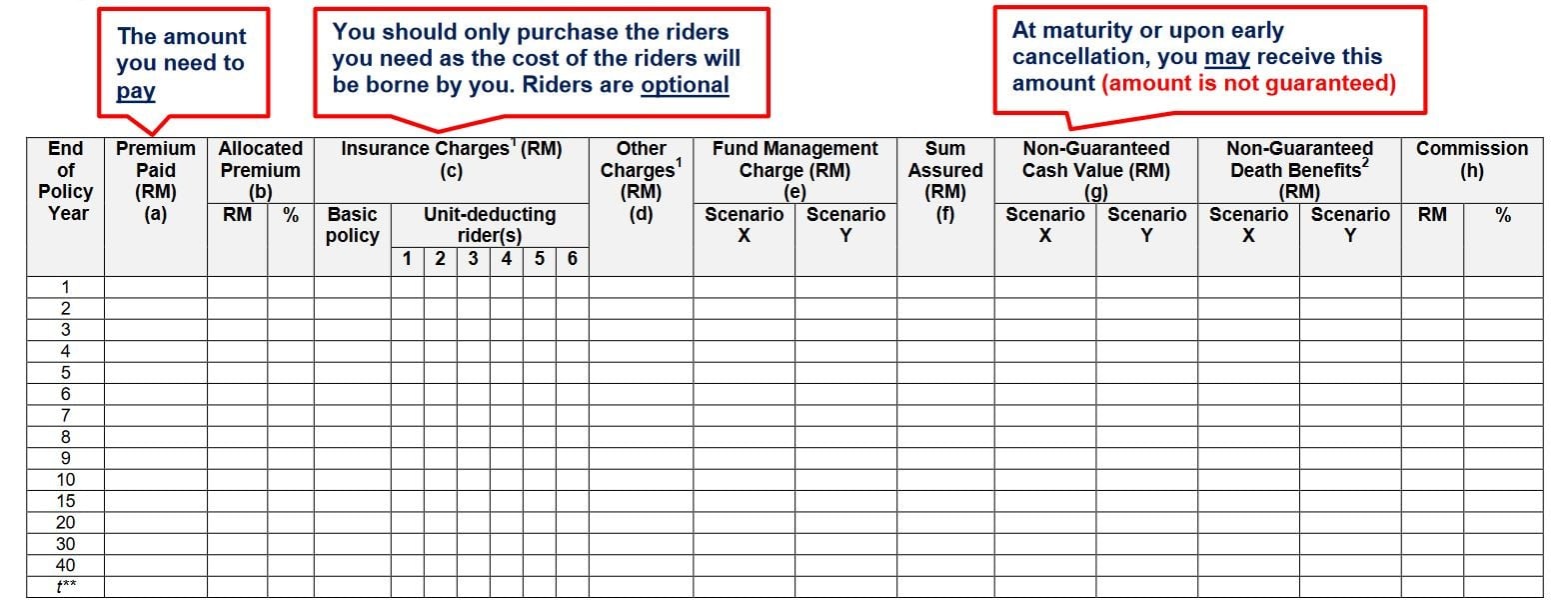

Product illustrations should be based on 2% and 5%

(Sample product illustration by Bank Negara)

(Sample product illustration by Bank Negara)

The regulations also introduce new rules for product illustrations at the point of sale so that the customer has an easier decision-making process. A product illustration is meant to show a potential ILP customer the possible movements of cash flows and the impact of fees and charges on cash values. Under the new rules, when illustrating hypothetical rates of return to a potential customer, insurers must base their illustrations on two types of rates: 2% and 5%.

Sample of a product illustration for an ILP policy that must be presented to an ILP customer at the point of sale. From 1 July, “Scenario X” must refer to return rates of 2%, while “Scenario Y” is set at a rate of 5%.

This is applicable for all types of funds except for equity funds, for which the rates should be 2% and the 10-year average historical FTSE Bursa Malaysia KLCI returns for the first 20 years and then 5% after that. According to Bank Negara, the 2% and 5% rates better demonstrate the interactions between cash flows without giving rise to undue expectations. These set rates should help paint a uniformly realistic picture to potential customers when deciding whether to take on an ILP policy.

All these new changes fall under Bank Negara’s overarching aim for investment-linked insurance products: to protect the interest of the consumers. From raising the MAR to improving transparency and standards of communication, these new regulations can hopefully help consumers to make better and more informed decisions regarding their ILP insurance policies.

The full Bank Negara policy document can be found on Bank Negara’s website.

About THE AUTHOR

Jacie Tan

Most Viewed Articles

Most Viewed Articles

Whole Life Insurance

Malaysia’s General Insurance Industry Posts RM1.2 Billion Underwriting Profit In 2025

Malaysia’s general insurance industry recorded an underwriting profit of RM1.2 billion in 2025, up RM125 million from the […]

Whole Life Insurance

More Certificate Holders Are Keeping Their Family Takaful Active In 2026

The takaful industry recorded total gross contributions of RM16.38 billion in 2025, up 4.73% year-on-year, according to the […]

Whole Life Insurance

U Mobile To Discontinue GoLife Insurance From 31 August 2026

U Mobile will stop offering its GoLife insurance service from 31 August 2026. If you’re already subscribed to […]

Comments (0)