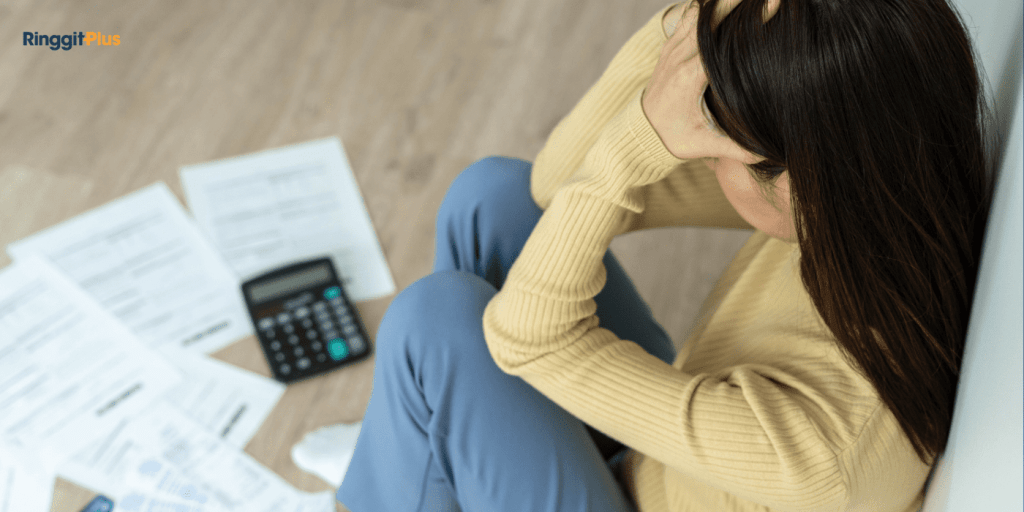

I stared at my banking app last month, and my stomach dropped. The numbers didn’t lie: I’d blown past my budget by RM1,000. Not because of an emergency or a major unexpected expense, but because of that familiar little voice in my head saying, “just one more thing.”

If you’ve ever fallen into this trap, you’re not alone. The year-end shopping season is particularly brutal for budgets. Between mega sales like 11.11 and Black Friday, festive preparations, and the general “treat yourself” atmosphere, my careful spending plan went out the window faster than you can say “Shopee flash sale.”

My Budget Plan: The 50/30/20 Rule

For the past year, I’d been following the 50/30/20 budgeting method, and honestly, it had been working well. The breakdown is simple: 50% goes to necessities like rent and utilities, 30% is for wants like eating out and shopping, and 20% goes to savings and debt repayment.

On my monthly salary, this system had been working perfectly. My 30% for wants covered regular meals out, entertainment subscriptions, occasional shopping trips, and a holiday fund I was building. Nothing extravagant, just normal life stuff that makes working hard feel worthwhile.

When The Shopping Season Hits

Then the year-end shopping season arrived, and my carefully balanced budget started cracking. It wasn’t one big purchase that did it. It was the death by a thousand small clicks.

First came the clothes shopping. I had legitimate reasons, or so I told myself. There were multiple dinners and gatherings coming up, plus I wanted to refresh my wardrobe before the new year. I couldn’t possibly wear the same outfit to everything, right? Uniqlo was having their sale, and before I knew it, I’d spent RM250 on new clothes. The logic was sound: buy now during the sale, save money in the long run. Classic justification.

Then the makeup. Oh, the makeup. I’d been eyeing a specific foundation for months, and suddenly it appeared in my feed with a 30% discount. RM150 gone in seconds. IT WAS ON SALE, which somehow made it feel like I was being financially responsible. Saving money by spending money. Makes perfect sense when you’re in the moment.

Gift shopping was the big one. Family birthdays, upcoming celebrations, and wanting to show appreciation to close friends; I didn’t want to look like the stingy relative or friend. RM500 disappeared across various purchases. A nice watch for my dad, perfume for my mum, toys for my younger brothers, and thoughtful gifts for close friends. Each purchase felt necessary and appropriate at the time.

But then came the real budget killer: the Shopee cart. It started innocently enough. I needed a new water bottle because mine had cracked. Fair enough. But while I was there, I saw this body wash everyone had been raving about online. Then some snacks that looked interesting. Before I knew it, I’d spent RM100 on miscellaneous items that weren’t really necessities, but weren’t exactly frivolous either. They lived in that dangerous grey zone between want and need.

The Moment Of Reckoning

When I finally tallied everything up, the damage was clear. My 30% allocation for wants had been completely obliterated. I’d gone over by approximately RM1,000.

The thing is, I wasn’t in actual financial trouble. My rent was paid, bills were sorted, and I wasn’t going to go hungry. But seeing that RM1,000 disappear from my carefully built-up savings felt awful. That money was supposed to be working towards my holiday fund, not covering impulse purchases I could barely remember making a week later.

None of these were terrible financial decisions on their own. I needed clothes for events. Gifts for family are part of maintaining relationships. The makeup was on sale. But together, they added up to a significant dent in my financial plans.

Managing The Mental Game Of Impulse Spending

After my spending spree, I’ve spent some time thinking about what went wrong and how to prevent it from happening again. Impulse spending isn’t about moral failing. It’s about understanding how our brains work and building systems that work with our psychology.

First thing: don’t beat yourself up. I overspent, but I didn’t ruin my life. I had emergency savings that could handle it, and that’s exactly what those savings are for. The shame spiral helps nobody.

The three-day rule has become my new best friend. When you see something you want to buy, wait three days. If you still want it after three days and can afford it, then buy it. A shocking number of “must-have” items lose their appeal once that initial dopamine hit wears off. That body wash and those snacks? Three days later, I wouldn’t have bothered.

I’ve also started separating my shopping funds more carefully. Instead of one big 30% allocation for “wants,” I’m breaking it down further. Specific amounts for clothes shopping, entertainment, eating out, and miscellaneous purchases. When the clothes budget is spent, it’s spent. No more borrowing from the entertainment fund to justify another shopping trip.

Pre-planning for expensive months has made a huge difference. The year-end period is always going to cost more. Major sales events, festive preparations, and gift-giving occasions all cluster together. Start setting aside money for these occasions months in advance. If I’d started a shopping fund in September, that extra RM1,000 wouldn’t have caught me off guard.

Looking Forward

My spending spree taught me that a good budget isn’t just about following the 50/30/20 rule. It’s about knowing your own spending patterns, recognising your weak points, and building systems that protect you from yourself.

The goal isn’t perfection. It’s sustainable financial health that lets you enjoy your money without derailing your future plans. If you need more budgeting guidance or want to find the best value deals to stretch your ringgit further, RinggitPlus has plenty of resources to help.

And the next big sale? I’ll be ready.

Follow us on our official WhatsApp channel for the latest money tips and updates.

As a creative content writer, Eloise has covered finance, business, lifestyle topics, and even moonlights as a singer-songwriter outside of RinggitPlus. Her current interests are learning the best ways to optimise spending and credit card hacks to gain more airline miles.

00votes

Article Rating

SHARE

About THE AUTHOR

Eloise Lau

Eloise Lau

As a creative content writer, Eloise has covered finance, business, lifestyle topics, and even moonlights as a singer-songwriter outside of RinggitPlus. Her current interests are learning the best ways to optimise spending and credit card hacks to gain more airline miles.

We provide weekly updates on every Friday at 5pm on the prices of RON95, RON97 and Diesel in Malaysia and a chart that shows the movement of fuel prices across a 6-week period. Bookmark this page now!

Subscribe to our exclusive weekly newsletter and we’ll bring you the week’s highlights of financial news, expert tips, guides, and the latest credit card and e-wallet deals.

Thank you for subscribing!

Stay tuned for what’s to come next in the personal finance world

Comments (0)