I Withdrew My EPF During COVID—Did I Ruin My Retirement?

RinggitPlus

22nd January 2026 - 5 min read

I didn’t think about retirement every day, but last week I finally checked my EPF balance after months of avoiding it.

The number was RM127,458. Not terrible, but it made me pause and think about how much higher it could have been if I hadn’t withdrawn money during COVID.

Before Everything Fell Apart

Before COVID, I was working as an events coordinator at a hotel in Kuala Lumpur, handling corporate conferences, product launches, and wedding receptions. The work was hectic and sometimes exhausting, but it was active and social, and there was always something happening.

I was earning RM8,000 a month, which, for a single guy in his late twenties, felt like I had finally found my footing.

I rented a studio in Petaling Jaya for RM1,800, had a manageable car loan, paid RM150 for a gym membership, and could meet friends for drinks without checking my bank balance first. I could even order the RM28 nasi lemak at a café without thinking too much about it.

I wasn’t living extravagantly or travelling constantly, but I was comfortable, and I assumed things would continue more or less the same way.

When Events Vanished Overnight

The events industry didn’t slow down during COVID. It stopped.

One week, I was coordinating a 300-person corporate conference, and the next, MCO was announced and every event on my calendar for the next six months was cancelled.

By mid-2020, the hotel could no longer justify the payroll, and in August, my boss called me in and gave me a choice. I could either take a pay cut to RM6,000 or accept a severance package and leave.

I chose the pay cut.

The Shift To RM6,000

Dropping from RM8,000 to RM6,000 didn’t feel too serious at first. In practice, it changed everything. The rent was still RM1,800, suddenly taking up more than a third of my income. My car loan was still RM980, even though I was barely driving. Insurance, phone bills, and utilities added up to roughly RM600, and groceries cost about RM800 if I was careful.

That left just over RM1,100 each month for savings or small comforts. For a guy who was used to more things and more money to spend, this was hard.

I tried to make it work by cancelling subscriptions, meal-prepping rice and chicken every Sunday, and working out at home. I didn’t have much of an emergency fund, so when my laptop died and I needed a refurbished one for work at RM2,400, it hit hard. It also made me realise how quickly financial pressure can build and how small buffers really make things easier.

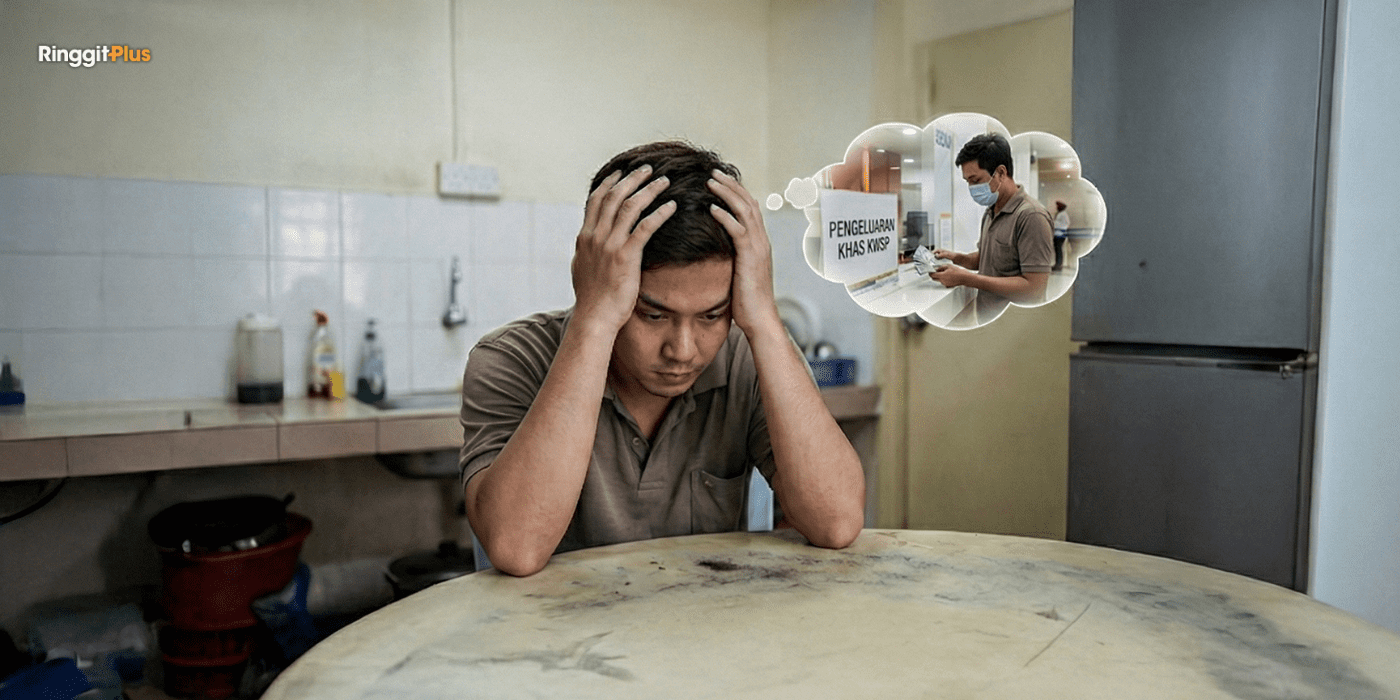

Touching My EPF

By January 2021, I had RM3,200 left in my bank account, and rent was due in two weeks. That’s when I started looking seriously at EPF withdrawal options.

The i-Sinar scheme allowed withdrawals of up to RM10,000 from Account 1 for people who had lost income during COVID, and I qualified.

EPF is meant for retirement, but at the time, I needed the money to get through the month. I remember filling out the application on my laptop, feeling uneasy about it, but also knowing I didn’t have many alternatives. Taking action was better than freezing in uncertainty. Eventually, I went through with a RM10,000 withdrawal.

It gave me some breathing room.

Building Stability And Planning Ahead

Events were slowly coming back at a smaller scale, but I had already seen how quickly the entire industry could disappear. I started applying to other roles and focused on industries that felt more stable, ones that would still function even during disruptions.

In December 2021, I accepted a logistics coordinator role at a manufacturing company with a monthly salary of RM6,500. Most of the work was still remote, but the pay was slightly better than my post-cut salary. Settling into the role, I realised that having steady work mattered just as much as the higher pay I had left behind. That made me start thinking seriously about my future and how to rebuild my finances.

On top of EPF, I considered PRS and other investments, but taking on more risk felt uncomfortable while my cash flow was still tight. Returning to the events industry could offer higher pay and faster EPF growth, but I realised I needed to focus on what I could control and build a foundation I could rely on.

So I decided to focus on building a small emergency fund first to give myself some financial cushion in case another unexpected expense came up. Once that was in place, I planned to start making voluntary EPF contributions of RM300 to RM500 a month to slowly rebuild my retirement savings.

Putting It In Perspective

Today, I earn RM8,200 a month, roughly the same amount I did before COVID. Some of my former colleagues stayed in events and are doing well, moving into senior roles, managing larger projects, or running their own companies. It’s natural to wonder “what if,” but comparing yourself constantly can be paralysing. Instead, I try to focus on what I can do now to make up for lost ground and secure my future.

At 34, I still have 21 years until 55, which is longer than I have been working so far. The EPF withdrawal and career switch set me back compared with where I might have been, but they did not ruin my future. The real mistake would be spending the next 20 years frozen by regret instead of taking action.

For anyone in their late 20s or 30s who withdrew EPF during COVID, the lesson is simple. One decision does not define your retirement. You still have time to recover, but only if you start now.

Follow us on our official WhatsApp channel for the latest money tips and updates.

About THE AUTHOR

RinggitPlus

Most Viewed Articles

Most Viewed Articles

Money Management

Government Boosts Co-Investment For SMEs With RM2 For RM1 Offer

The Investment, Trade and Industry Ministry (MITI) and the Securities Commission (SC) have launched a new Smart Manufacturing […]

Money Management

4 Money Mistakes In Your 20s That Hurt In Your 30s

When you are in your 20s, it is easy to feel like the future is too far away […]

Comments (0)