Employees with a side business need to file their taxes differently from those with salary income alone. In Malaysia, side income is declared separately and treated as business income, which comes with its own filing form, its own deadline, and its own set of deductions.

Because business expenses can be claimed against your gross earnings, tax is calculated on your net income rather than everything you brought in. Equipment, platform fees, and marketing costs all count, and they can bring your taxable amount down considerably.

LHDN classifies income from a consistent activity as business income, not “other income.” Selling products, providing services, or taking on freelance projects all qualify, while a one-off sale of personal belongings doesn’t.

Form B, Not Form BE

Employees who have no business income file and only earn a salary use Form BE. Once you have side business income, regardless of whether you’re formally registered as a sole proprietor, you need to file Form B instead. Form B covers both your employment and business income in a single filing, so you don’t need to submit Form BE separately.

This is one of the most common points of confusion for salaried workers with side gigs. Form BE only covers employment income and passive income like dividends and rental. The moment you have business income that is not a salary from your employer, LHDN requires Form B, which includes a dedicated section (Part 4) for business and partnership income.

Form B also has a later filing deadline than Form BE. For YA 2025, the e-Filing deadline for Form B is 30 June 2026, compared to 30 April 2026 for Form BE.

SSM Registration Is Not A Requirement

You can declare side business income on Form B without being registered with SSM (Companies Commission of Malaysia) as a sole proprietor. LHDN and SSM are separate, and your tax obligations don’t depend on your SSM registration status.

That said, registering with SSM has practical advantages. A registered business name makes it easier to open a business bank account, issue official invoices, and claim certain expenses. Registration costs a nominal annual fee.

If you’re already registered with SSM, use your business registration number when filing. If you’re not, you can still declare your income as an unregistered sole proprietor. Just report the income and expenses honestly under your own name.

What Counts As Allowable Business Expenses

As a business income earner, you can deduct legitimate business expenses from your gross income before tax is calculated. Only the net profit is subject to tax, meaning revenue after allowable expenses have been deducted.

Expenses must be wholly and exclusively incurred in producing your business income to qualify. Common allowable deductions include:

Cost of goods sold: materials, products, or inventory purchased to fulfil orders

Platform and transaction fees: marketplace commissions and payment gateway charges

Equipment and tools: laptops, cameras, software subscriptions, or other tools used for the business (if an item is also used personally, only the business-use portion is deductible)

Advertising and marketing: paid ads, printing, or promotional materials

Transportation: fuel or toll costs for business activities such as deliveries or client visits

Professional services: accounting or legal fees related to your business

Personal expenses dressed up as business costs, fines or penalties, and capital expenditure are not deductible, though capital allowances may apply for qualifying assets.

Keep receipts and records for at least seven years. LHDN can audit past years, and documentation for every claim protects you if questions arise later.

How Your Side Income Affects Your Overall Tax

Your employment income and business income are added together to determine your chargeable income for the year. Malaysia uses a progressive tax rate, so a higher combined income means a larger slice is taxed at a higher rate.

Take a salary that puts your chargeable income at RM70,000. You’re paying 11% on the portion between RM50,001 and RM70,000. If your side business adds another RM20,000 in net profit, that extra RM20,000 falls into the next bracket and gets taxed at 19%. The difference isn’t dramatic, but it’s worth factoring in when pricing your services or planning your expenses.

All the usual personal reliefs still apply when filing Form B, including lifestyle relief, medical relief, EPF contributions, and so on. These reduce your chargeable income across both income streams.

MTD/PCB And Why You May Still Owe Tax

If you’re an employee, your employer deducts Monthly Tax Deductions (MTD, also known as PCB) from your salary throughout the year. This covers your employment income only, and your side business income isn’t factored in at all.

MTD deducted correctly every month still won’t account for side business income, so there will almost certainly be additional tax to pay when you file. The amount owed is calculated when you complete Form B and compare your total tax liability against what was already deducted via MTD.

LHDN allows you to settle the balance by the filing deadline. If the amount is substantial, you can also make advance payments through MyTax to spread the liability across the year rather than paying a lump sum at filing time.

If you consistently owe a large amount at year-end, LHDN may ask you to make estimated tax payments via CP500 instalments the following year. It is a scheduled payment system for individuals with business income, not a penalty, but it does require budgeting for those payments throughout the year.

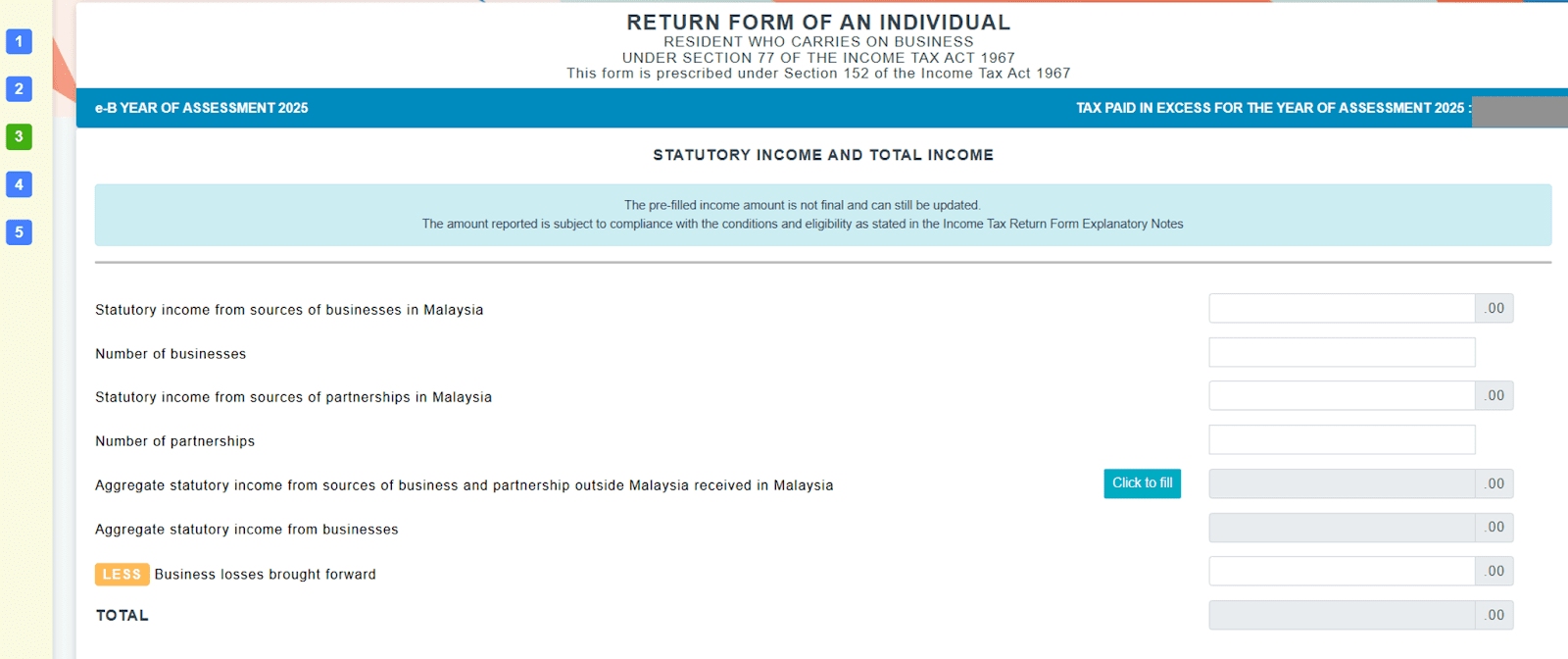

Under Statutory Income from Sources of Businesses in Malaysia, enter your gross business income, allowable expenses, and the resulting adjusted income:

Claim your reliefs, check your tax payable, and submit before 30 June 2026.

For straightforward cases, such as a handful of freelance projects with no employees or major asset purchases, the business income section can be completed without a separate set of accounts. A simple record of your invoices and expenses for the year is enough; just transfer the totals into the relevant fields.

For more complex situations, such as a business with significant inventory, multiple income streams, or capital assets, it may be worth engaging a tax agent to make sure the figures are reported correctly.

A Quick Recap

Form BE

Form B

Who uses it

Employees with no business income

Employees with side business income

e-Filing deadline (YA 2025)

30 April 2026

30 June 2026

Can claim business expenses

No

Yes

MTD covers full tax liability

Usually

No (side income creates additional tax)

The main thing to remember is that side income isn’t a grey area. It belongs on your tax return, and filing it correctly, with legitimate expenses deducted, keeps you compliant with LHDN and often reduces the amount you actually owe.

***

If you’re also earning returns from investments, our guide to investment income and tax in Malaysia breaks down what’s taxable and what isn’t.

Follow us on our official WhatsApp channel for the latest money tips and updates.

Steffi Manisha Arokiam is a Tax Director at ThinkTX Consultants, where she leads the firm’s Transfer Pricing and e-Invoicing practice. She advises both individuals and corporations across a wide range of tax matters, including Real Property Gains Tax (RPGT), stamp duty, estate tax, and global mobility for expatriates. Recognised for combining strong technical expertise with a practical, solutions-driven approach, Steffi helps clients navigate complex tax issues with clarity and confidence.

A respected thought leader in taxation, Steffi has authored numerous technical articles and professional newsletters. Her work has been published by the International Bureau of Fiscal Documentation (IBFD) and Wolters Kluwer (CCH), and she has been featured on BFM 89.9 discussing crypto taxation.

Professional Affiliations

Member of the Malaysian Institute of Accountants (MIA)

Member of the Chartered Tax Institute of Malaysia (CTIM)

ASEAN Chartered Professional Accountant (ASEAN CPA)

Member of the International Fiscal Association (IFA)

Professional Trainer certified by HRD Corp

As a trusted tax partner of RinggitPlus, Steffi reviews and verifies all content relating to Malaysian taxation to ensure it is accurate, up to date, and practical — helping readers better understand the tax system and make the most of their tax position.

00votes

Article Rating

SHARE

About THE AUTHOR

Steffi Manisha Arokiam

Steffi Manisha Arokiam

Steffi Manisha Arokiam is a Tax Director at ThinkTX Consultants, where she leads the firm's Transfer Pricing and e-Invoicing practice. She advises both individuals and corporations across a wide range of tax matters, including Real Property Gains Tax (RPGT), stamp duty, estate tax, and global mobility for expatriates. Recognised for combining strong technical expertise with a practical, solutions-driven approach, Steffi helps clients navigate complex tax issues with clarity and confidence.

A respected thought leader in taxation, Steffi has authored numerous technical articles and professional newsletters. Her work has been published by the International Bureau of Fiscal Documentation (IBFD) and Wolters Kluwer (CCH), and she has been featured on BFM 89.9 discussing crypto taxation.

Professional Affiliations

Member of the Malaysian Institute of Accountants (MIA)

Member of the Chartered Tax Institute of Malaysia (CTIM)

ASEAN Chartered Professional Accountant (ASEAN CPA)

Member of the International Fiscal Association (IFA)

Professional Trainer certified by HRD Corp

As a trusted tax partner of RinggitPlus, Steffi reviews and verifies all content relating to Malaysian taxation to ensure it is accurate, up to date, and practical — helping readers better understand the tax system and make the most of their tax position.

Subscribe to our exclusive weekly newsletter and we’ll bring you the week’s highlights of financial news, expert tips, guides, and the latest credit card and e-wallet deals.

Thank you for subscribing!

Stay tuned for what’s to come next in the personal finance world

Comments (0)