If you earned around RM38,000 in 2025, income tax probably is not about managing a large bill; it is about recovering any excess tax paid. If your employer has been deducting MTD from your monthly salary throughout 2025, filing your income tax return correctly and claiming every relief you are entitled to will likely result in a full refund of whatever was withheld.

That is not a small thing. Once personal relief, EPF contributions, lifestyle purchases, and insurance premiums are taken into account, your chargeable income could fall below the taxable threshold, meaning income tax may not apply at all and every ringgit deducted could be refunded.

Tax returns for income earned between 1 January and 31 December 2025 must be submitted in 2026 through LHDN’s MyTax portal. Miss the deadline or skip the filing entirely, and you do not just lose the refund — you risk a penalty on top of it.

This guide walks through the full filing process: who needs to file, the current tax rates, every major relief available, how to submit through MyTax, and what to do if something goes wrong after you have filed.

Who Needs to Pay Income Tax in Malaysia?

Income tax applies to individuals whose annual income exceeds the taxable threshold.

You are required to file if you fall into any of the following categories:

Individuals whose taxable income exceeds the minimum taxable threshold under the Income Tax Act 1967

Salaried employees

Self-employed individuals, freelancers, or business owners with taxable income

Foreigners who have worked in Malaysia

Even if your employer has deducted MTD from your salary, you must still file an income tax return if your income exceeds the threshold.

Failure to file may result in penalties under the Income Tax Act 1967.

Malaysia Personal Income Tax Rates for YA 2025

Malaysia operates a progressive tax system. This means income is taxed in tiers, and only the portion within each band is taxed at the corresponding rate.

Resident individual tax rates for YA 2025 remain progressive, starting from 0% for lower income brackets and increasing for higher income levels.

Your tax payable depends on your chargeable income, which is calculated as:

Chargeable Income (RM)

Calculations (RM)

Rate %

Tax (RM)

0 – 5,000

On the first 5,000

0

0

5,001 – 20,000

On the first 5,000Next 15,000

1

0150

20,001 – 35,000

On the first 20,000Next 15,000

3

150450

35,001 – 50,000

On the first 35,000Next 15,000

6

600900

50,001 – 70,000

On the first 50,000Next 20,000

11

1,5002,200

70,001 – 100,000

On the first 70,000Next 30,000

19

3,7005,700

100,001 – 400,000

On the first 100,000Next 300,000

25

9,40075,000

400,001 – 600,000

On the first 400,000Next 200,000

26

84,40052,000

600,001 – 2,000,000

On the first 600,000Next 1,400,000

28

136,400392,000

Exceeding 2,000,000

On the first 2,000,000Every next ringgit

30

528,400………..

For example, if your chargeable income is RM48,000, your tax is calculated progressively across the relevant brackets. If you successfully claim RM13,500 in reliefs and reduce your chargeable income to RM34,500, you will enjoy a tax rebate of RM400.

Understanding how progressive tax works helps you plan your relief claims more effectively.

Tax Filing for Foreigners

Foreigners working in Malaysia are taxed according to their residency status.

Individuals who stay in Malaysia for 182 days or more in a calendar year are treated as tax residents. They are taxed at progressive resident rates and are eligible to claim tax reliefs and rebates.

Individuals who stay fewer than 182 days but work for at least 60 days are classified as non-residents. Non-residents are generally taxed at a flat rate of 30% on employment income and are not eligible for tax reliefs.

Summary Of Residency Treatment

Residency Status

Days In Malaysia

Tax Treatment

Relief Eligibility

Resident

182 days or more

Progressive rates

Yes

Non-resident

Fewer than 182 days

30% flat rate

No

Foreigners are not taxed in Malaysia if they work lesser than 60 days, receive qualifying pensions, earn Malaysian bank interest, or receive tax-exempt dividends.

Residence status directly affects both tax rates and eligibility for tax reliefs.

How to File Income Tax in Malaysia

The form you use depends on your income source.

Form M – Non-residents

Form BE – Resident individuals without business income

Form B – Resident individuals carrying on a business

Filing Deadlines

Statutory filing deadlines under the Income Tax Act 1967 are as follows:

Form BE (resident individuals without business income)

30 April 2026

Form B (resident individuals carrying on a business)

30 June 2026

LHDN typically grants an administrative extension for e-Filing submissions each year. For YA 2025, the extended e-Filing deadlines are as follows:

Form BE (e-Filing)

15 May 2026

Form B (e-Filing)

15 July 2026

Taxpayers should always refer to LHDN’s official announcements for confirmation of the extended e-Filing dates.

All submissions must be completed electronically through MyTax.

Step-by-Step Guide to Filing via MyTax

1. Registering as a First-Time Taxpayer

If you are filing for the first time, you must:

Register via e-Daftar on the MyTax portal

Obtain a Tax Identification Number. This confirms that you are a registered taxpayer in Malaysia.

Request a one-time PIN for e-Filing activation. This allows you to access the e-Filing platform, where you will submit your Income Tax Return Form (ITRF).

The PIN can be obtained online or at an LHDN branch.

Accessing e-Filing and Selecting the Correct Form

If you are an existing taxpayer, you can skip the registration process and log in directly to the MyTax portal to access e-Filing and submit your Income Tax Return Form.

One useful feature of the MyTax portal is the language toggle option, which allows you to switch between Bahasa Malaysia and English. If you are more comfortable in one language, adjust this setting before you begin to make the process smoother.

How to Access e-Filing via MyTax

Log in to your MyTax account using your registered credentials.

Once inside your dashboard, you will see key information such as your tax balance or refund amount.

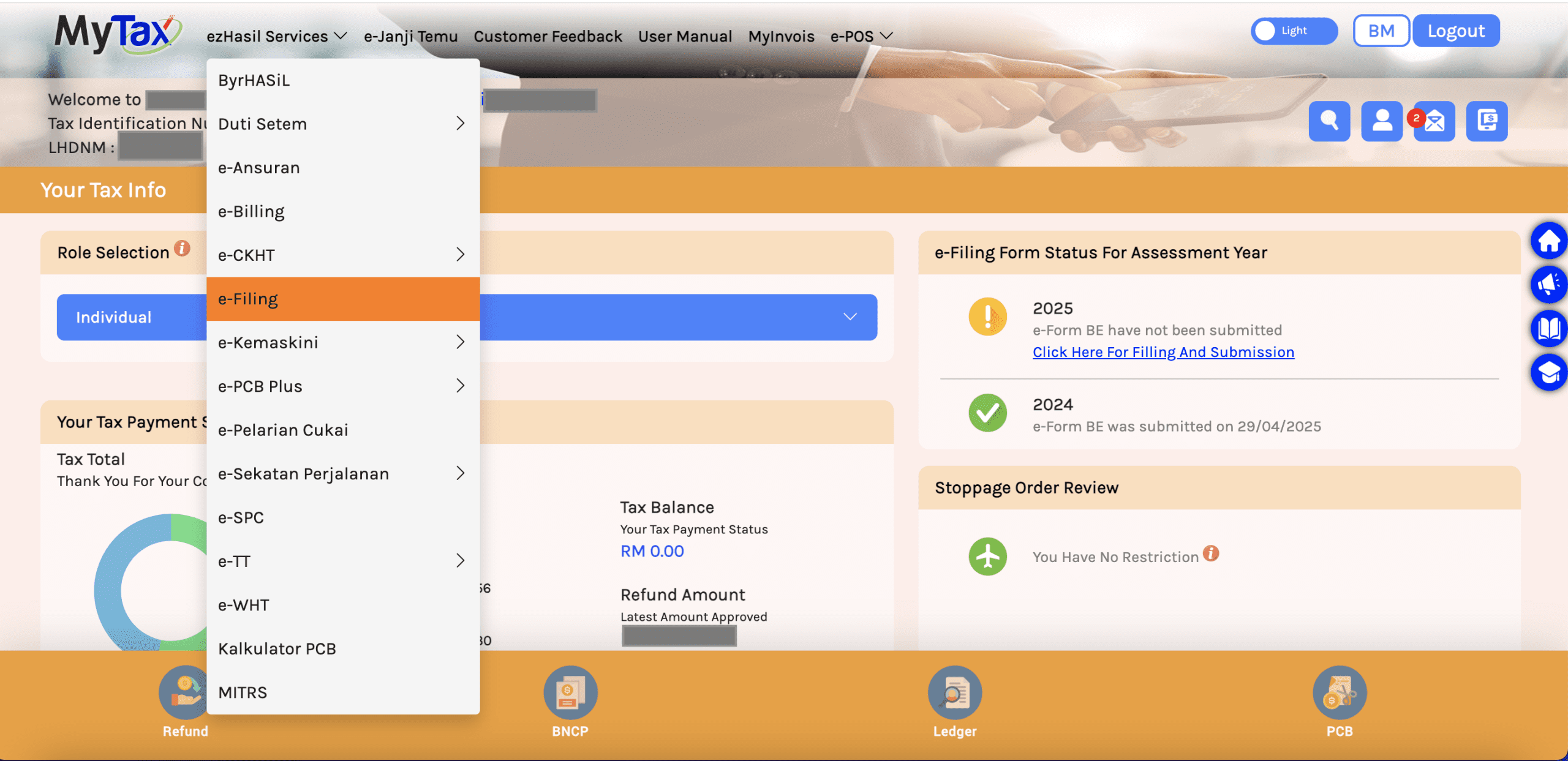

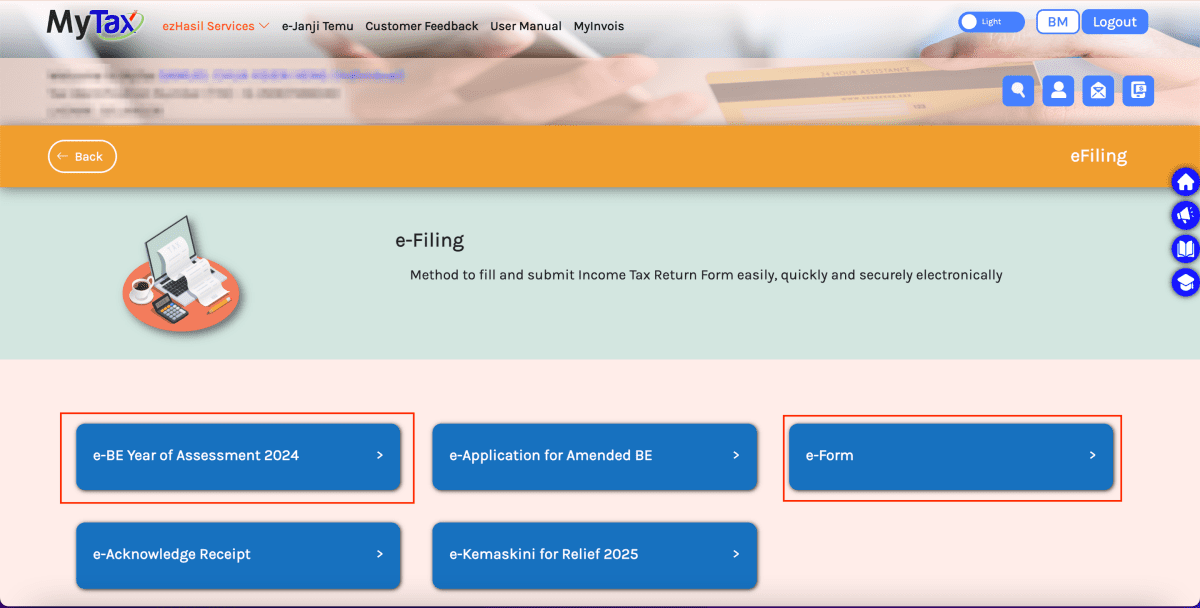

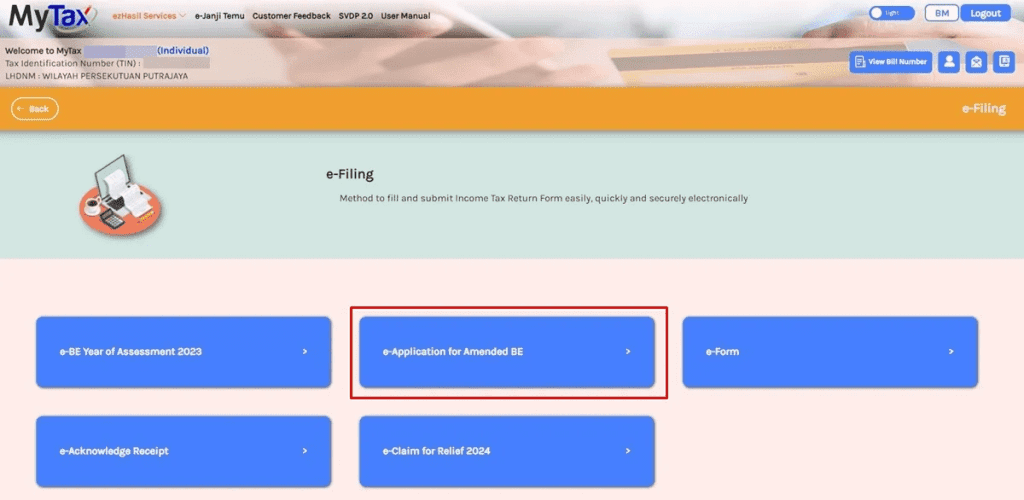

Navigate to “EzHasil Services” and select “e-Filing”.

Choose the appropriate Income Tax Return Form for YA 2025.

If your income source has changed, for example, from salaried employment to running a business, you may not see a quick access link. In this case, select “e-Form” to manually choose the correct return form.

Always ensure that you select YA 2025, which corresponds to income earned during the taxable period from 1 January to 31 December 2025.

Choosing the Correct Income Tax Return Form

As you make your selection, ensure that you choose the correct form based on your income category.

If your income type has changed during the year, such as moving from salaried employment to operating a business, you must select the appropriate form accordingly.

You can find a full list of other return forms, including those for partnerships, associations, and estates of deceased persons, on the official LHDN website.

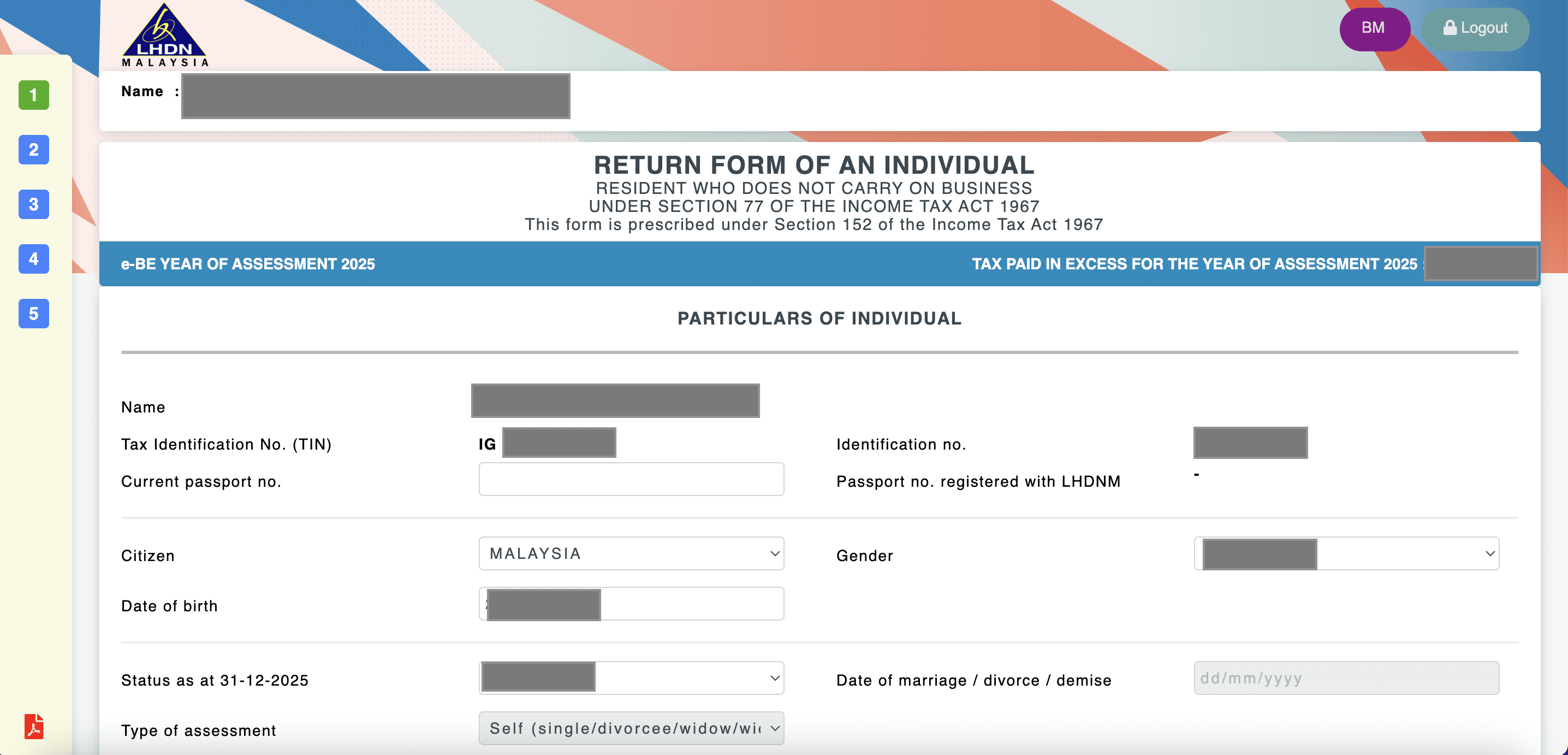

Filling in Your Income Tax Return Form

Once you have selected the correct form for YA 2025, the system will bring you to your Income Tax Return Form. The form is divided into several sections. It is important to complete each part carefully before proceeding to the next.

To make it easier, we will break it down section by section, guiding you through each part of the form so that you can complete your tax filing accurately and efficiently.

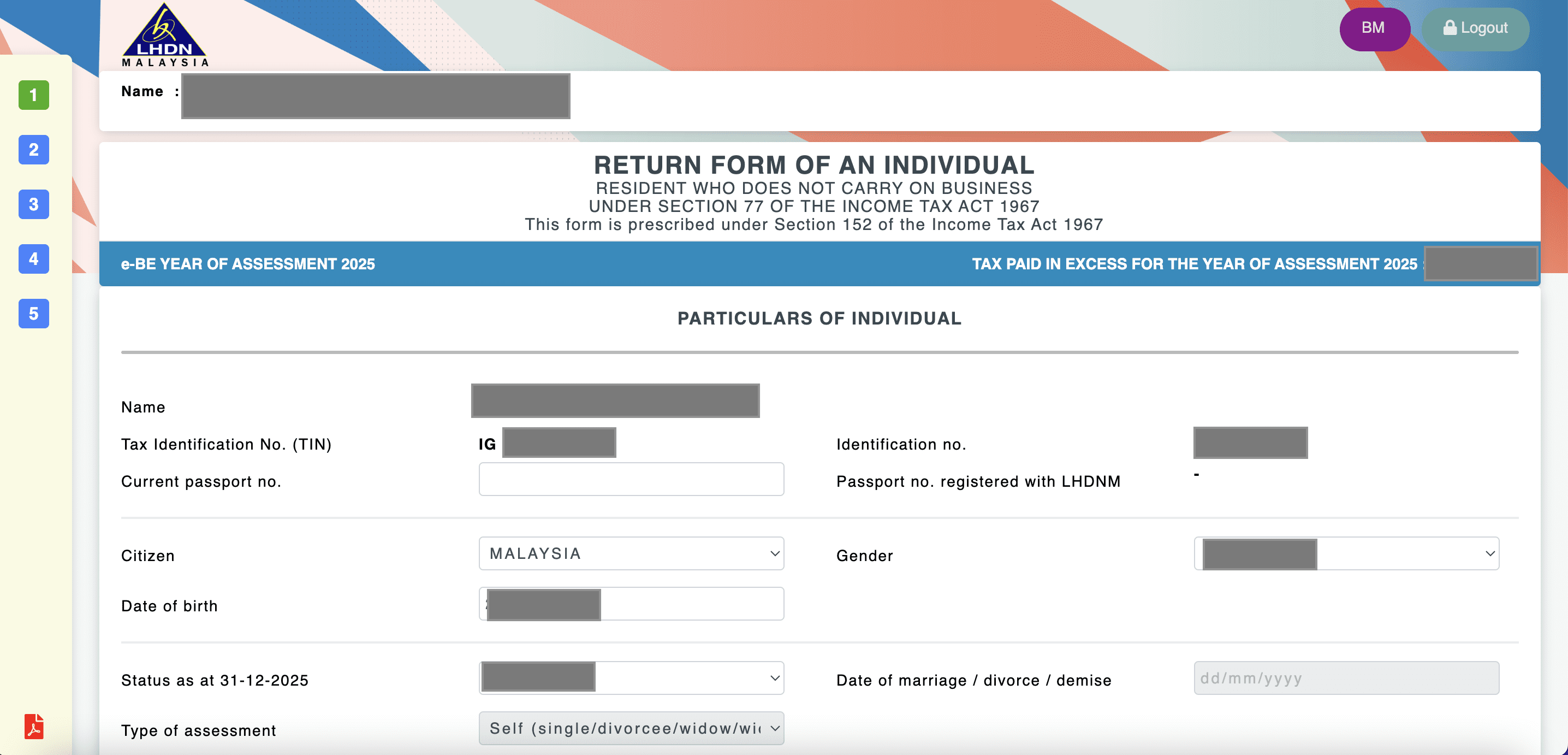

i) Particulars of Individual

The first section captures your personal information. Some details, such as your identification number and name, will already be pre-filled based on LHDN’s records. However, you should still review all information carefully to ensure there are no errors.

Pay attention to:

Residential address

Email address

Marital status

Type of assessment

If you are married, you must choose between joint assessment and separate assessment.

Under joint assessment, one spouse declares the combined income of both spouses. Under separate assessment, each spouse files their own tax return. The option selected can affect eligibility for spouse relief and may change the total tax payable, so choose the arrangement that is more beneficial for your situation.

Once everything is confirmed, proceed to the next section.

ii) Other Particulars

This section builds on your personal details and focuses on contact information, refund payment methods, and a few administrative declarations.

Make sure your bank account number is correct, as this is where tax refunds will be credited. If you prefer to receive refunds via DuitNow, select it under the “Method of payment for tax refund” field and complete the required details. An error here can delay refund processing, even if the rest of your tax return is accurate.

If you changed employers during 2025, update the Employer’s Number accordingly. This helps ensure your employment details align with the information reported through your EA form and MTD. You should also confirm whether your employer bears your tax, which may apply if your compensation package includes a tax allowance or if your employer has agreed to cover your tax liability. If this applies, make sure you tick “Yes” under “Tax borne by employer”, as it affects your declaration.

You may also see fields relating to asset disposal, including disposals that fall under the Real Property Gains Tax Act 1976. If you sold a property or disposed of certain assets during 2025, provide the required details. Even though Real Property Gains Tax is assessed separately, the declaration in your return should still be accurate.

In some cases, the form may include a section for incentive claims under paragraph 127(3)(b) and subsection 127(3A), which covers tax exemptions granted under specific gazette orders or exemptions issued by the Minister of Finance. If you are not claiming any such incentive, you can leave this section blank.

Once you have reviewed and completed these fields, move on to the income declaration section.

iii) Declaring Your Income

This is the main section of your Income Tax Return Form, where you declare all statutory income earned between 1 January and 31 December 2025.

For most salaried individuals, your EA form will be the primary reference document. The EA form summarises your annual employment income, allowances, bonuses, benefits, and the total MTD deducted by your employer throughout the year.

When completing this section, ensure that you enter:

Gross employment income

Bonuses and commissions

Taxable allowances

Benefits-in-kind and perquisites, where applicable

While your EA form provides a structured summary, you remain responsible for ensuring that the figures entered are accurate and complete.

If you earned income apart from your salary, you must also declare it in the appropriate sections. This includes income such as rental from property, freelance or part-time work, royalties, pensions, commissions, or any other taxable earnings.

For example, if you occasionally undertake freelance design, lecturing, writing, or consulting work, the income received must be declared even if it was not subject to MTD.

At the same time, certain types of income may qualify for exemption under Malaysian tax laws. These may include specific allowances, certain benefits-in-kind within prescribed limits, tax-exempt dividends, or foreign-sourced income that qualifies for exemption under prevailing rules. Only exclude income if you are certain it meets the exemption criteria.

After all relevant income figures are entered, the system will automatically calculate your aggregate income.

You will then need to enter the total amount of MTD, also known as Potongan Cukai Bulanan, as reflected on your EA form. This represents your advance tax paid throughout the year and will be offset against your final tax payable.

If the total deduction exceeds your final tax liability, you will be entitled to a refund. If it is lower, you will need to settle the balance.

Claiming Tax Reliefs and Rebates

Once your income has been declared, you will move on to claiming tax reliefs. This is where careful record-keeping throughout the year becomes important.

Tax reliefs reduce your chargeable income, which in turn lowers the tax bracket your income falls into. The more eligible reliefs you claim, the lower your chargeable income will be.

Below is the full list of tax reliefs available to resident individuals for YA 2025.

Category

Details / Eligible Expenses

Relief Limit

INDIVIDUAL

Individual & Dependent Relatives

Self and dependent relatives

RM9,000

Disabled Individual

Additional relief for disabled individuals

RM7,000

Husband / Wife / Alimony Payments

Spouse or alimony payment relief

RM4,000

Disabled Husband / Wife

Additional relief for disabled spouse

RM6,000

Education Fees

Tertiary level (other than Master’s/PhD); Master’s Degree / Doctor of Philosophy

RM7,000

Skills Enhancement / Personal Development Courses

Restricted to approved skills & personal development courses

RM2,000

Interest on Housing Loan – First Home Ownership

Sales & Purchase Agreement from 1 Jan 2025 to 31 Dec 2027. • House price up to RM500,000: RM7,000 • House price RM500,001–RM750,000: RM5,000

RM7,000 / RM5,000

MEDICAL & SPECIAL NEEDS

Self / Spouse / Child – Medical

Serious illness; Fertility treatment; Vaccination (up to RM1,000); Dental exam & treatment (up to RM1,000); Medical exam (up to RM1,000) incl. full check-up, disease screening, mental health screening, self-health monitoring equipment, self-testing kits; Learning disability diagnosis/intervention for child aged ≤18 (up to RM6,000)

RM10,000

Parents & Grandparents

Medical treatment, dental treatment, special needs & care; Full medical check-up & vaccination (up to RM1,000)

RM8,000

Basic Support Equipment for Disabled Individual

Self / Spouse / Child / Parent

RM6,000

LIFESTYLE

Lifestyle

Self / Spouse / Child: • Purchase/subscription of reading materials • Personal computer / smartphone / tablet • Internet subscription bills • Skills enhancement / self-development course fees

RM2,500

Lifestyle – Additional (Sports)

• Purchase of sports equipment • Rental/entrance fees to sports facilities • Sports competition registration fees • Gym membership / sports training fees

RM1,000

Electric Vehicle Charging Equipment & Domestic Food Waste Composting Machine

Additional Relief – Child with Disabilities Aged 18+

Unmarried; Full-time instruction (Diploma & above in Malaysia / Degree & above outside Malaysia)

RM8,000

Registered Childcare Centre (TASKA) / Kindergarten (TADIKA) Fees

Child aged 6 and below; claimable by husband / wife

RM3,000

Purchase of Breastfeeding Equipment

Female taxpayer only; Child aged ≤2 years; Allowed once every 2 years of assessment

RM1,000

Disclaimer: This table is a summary only. For full details, visit www.hasil.gov.my.

After entering all eligible reliefs, the system will automatically calculate your chargeable income. This final figure determines which tax bracket applies to you and how much tax you are required to pay.

In some cases, reducing your chargeable income may even move you into a lower tax band, lowering your overall tax liability.

It is also important to understand that tax rebates work differently. Unlike reliefs, which reduce your income, rebates are deducted directly from your final tax amount.

For YA 2025, individuals with chargeable income not exceeding RM35,000 may qualify for a RM400 rebate. Zakat and fitrah contributions may also be claimed as rebates, capped at the total tax payable.

To see how this works in practice, consider the following example.

Suppose your total income for YA 2025 is RM50,000 and you claim RM15,000 in tax reliefs. This reduces your chargeable income to RM35,000.

At RM35,000, your total tax payable would amount to RM600 under the progressive tax structure.

Because your chargeable income is RM35,000, you qualify for the RM400 individual rebate, as the rebate applies to resident individuals whose chargeable income does not exceed RM35,000. This reduces your tax payable from RM600 to RM200.

If you also contributed RM400 in zakat during the year, you may claim it as a rebate, subject to the total tax payable. In this example, since your tax payable after the individual rebate is RM200, only RM200 of zakat can be utilised. Your final tax payable would therefore be reduced to nil, and any excess zakat rebate cannot be refunded.

Understanding how reliefs and rebates work allows you to plan your tax position more effectively and avoid unnecessary overpayment.

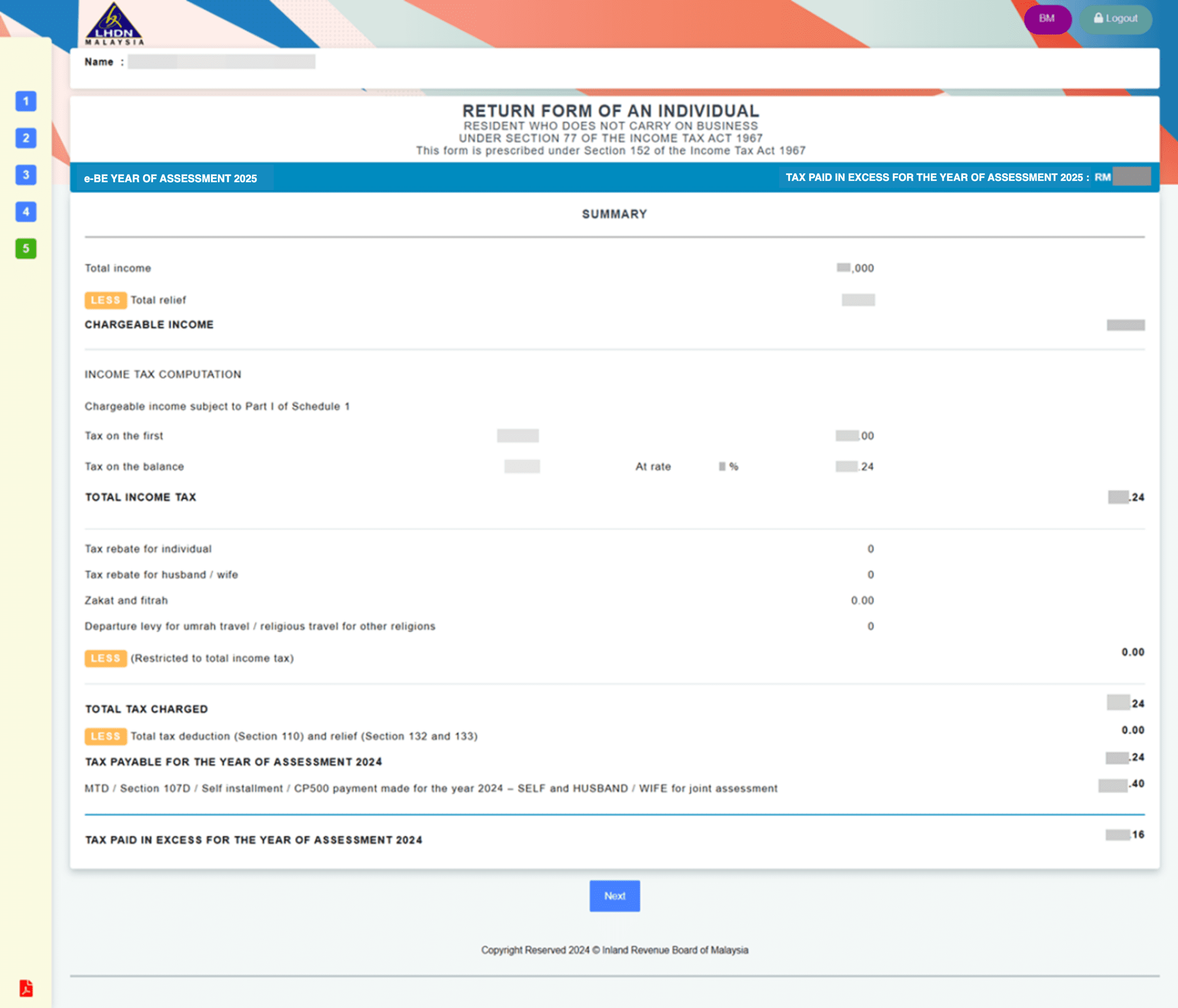

Checking and Submitting Your Return

Once you reach the summary page, you are almost done.

This page shows your final tax computation, including your total income, total reliefs claimed, chargeable income, tax payable, and any balance to be paid or refunded.

If the final amount is in a refund position, it simply means you have paid more tax through MTD than required, and you are entitled to receive the refund.

Take a few minutes to review everything carefully. Compare the figures against your EA form and receipts to ensure nothing has been missed. If you notice any errors, you can return to the relevant sections of your Income Tax Return Form and make corrections. The system will automatically recalculate your tax once changes are made.

When you are satisfied that all information is accurate, proceed to the declaration page.

A pop-up window may appear asking you to confirm your identification number and password. Ensure your browser allows pop-ups so the process is not interrupted. Once confirmed, click “Sign” to complete your submission.

After successful submission, a confirmation page will be displayed.

Before logging out, download and save:

The acknowledgement receipt

A copy of your submitted Income Tax Return Form

Under Section 82A of the Income Tax Act 1967, taxpayers are required to retain records for 7 years from the end of the relevant year of assessment.

Once that is done, your filing for YA 2025 is completed.

Amending Your Income Tax Form

Even with careful filing, mistakes can happen. If you realise that you made an error after submitting your Income Tax Return Form, corrections are still possible.

The type of amendment depends on the nature of the error and when it is discovered.

Online Amendments via e-Filing

For certain types of errors, amendments can be made online through MyTax.

This option is available only for:

Over-declared income

Under-claimed tax reliefs or tax rebates

You must have submitted your original BE Form before the filing deadline to qualify.

The e-Application for Amended BE is typically made available from 1 April for a limited period, subject to LHDN’s guidelines for the relevant year.

To amend online:

Log in to your MyTax dashboard

Select e-Filing

Click “e-Application for Amended BE”

Enter the corrected figures

Submit the amendment

The system will automatically recalculate your tax position.

Written Appeal for Other Errors

If the mistake does not fall under the online amendment category, you must submit a written appeal.

This generally applies to:

Under-declared or undeclared income

Overclaimed expenses or deductions

Incorrect reporting of taxable items

To correct:

Print your submitted e-Form

Clearly mark and initial each correction

Recalculate the tax manually

Prepare a formal appeal letter explaining the changes

Attach supporting documents such as EA forms and tax relief receipts

Submit it to the LHDN branch handling your tax file

Each appeal is subject to review and approval by LHDN.

Amended Return Form Within Six Months

If you discover an error after the filing deadline, you may submit an Amended Return Form within six months from the original submission deadline.

This option is available only if the original tax return was filed on time.

The Amended Return Form is typically required for cases involving:

Under-declared income

Overclaimed reliefs or incentives

The form must be submitted to the LHDN branch managing your tax file.

Paying Your Income Tax

After submission, you will either be entitled to a refund or required to settle the outstanding tax.

You Are Eligible for a Tax Refund

If your MTD exceeds your final tax liability, you are entitled to a refund.

Refunds are credited to the bank account provided in your tax return.

According to LHDN’s Client Charter:

Refunds are processed within 30 working days after e-Filing submission, subject to verification

Refunds for manual submissions may take up to 90 working days

Processing is subject to verification and may take longer if additional documents are required.

You Have Outstanding Tax to Pay

If your tax calculation shows a balance payable, you must settle it before the deadline to avoid penalties.

Malaysia operates under a Self-Assessment System. Taxpayers are responsible for computing and declaring their own tax correctly.

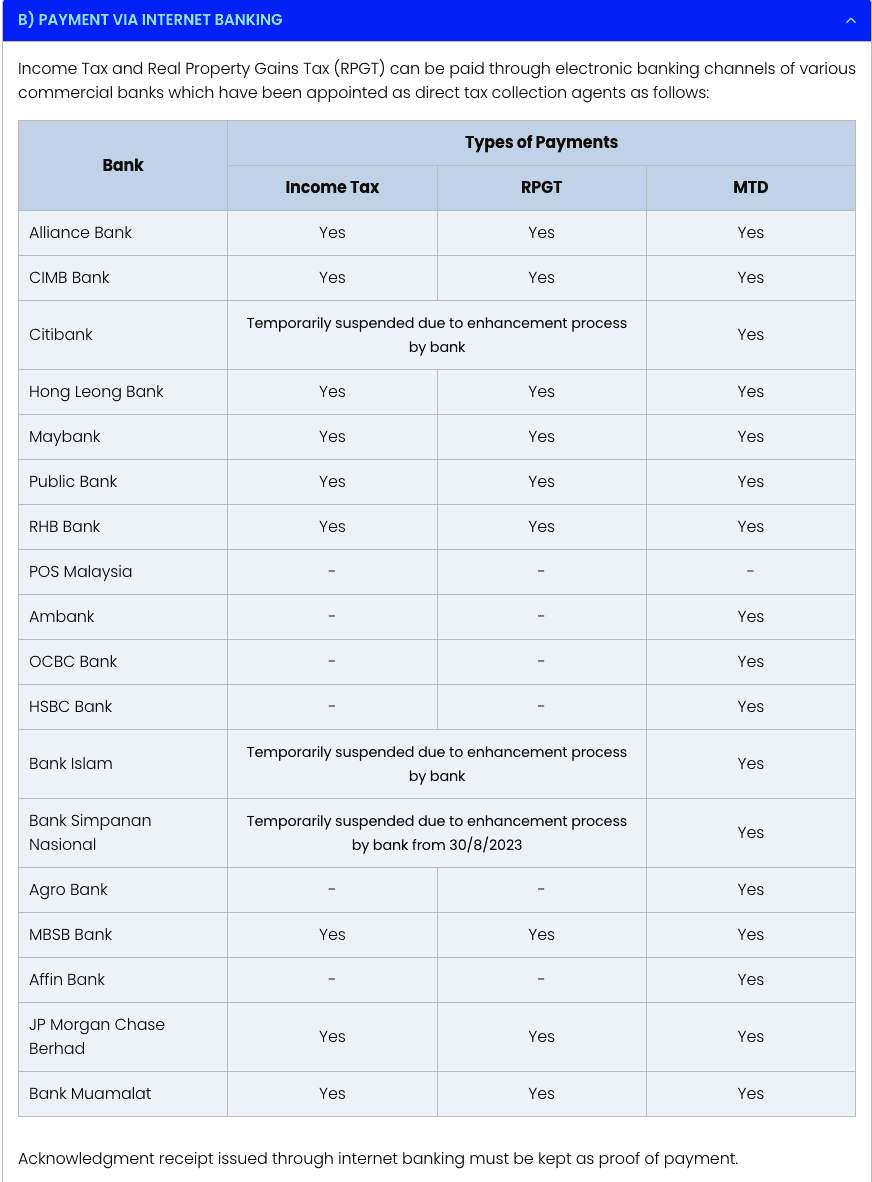

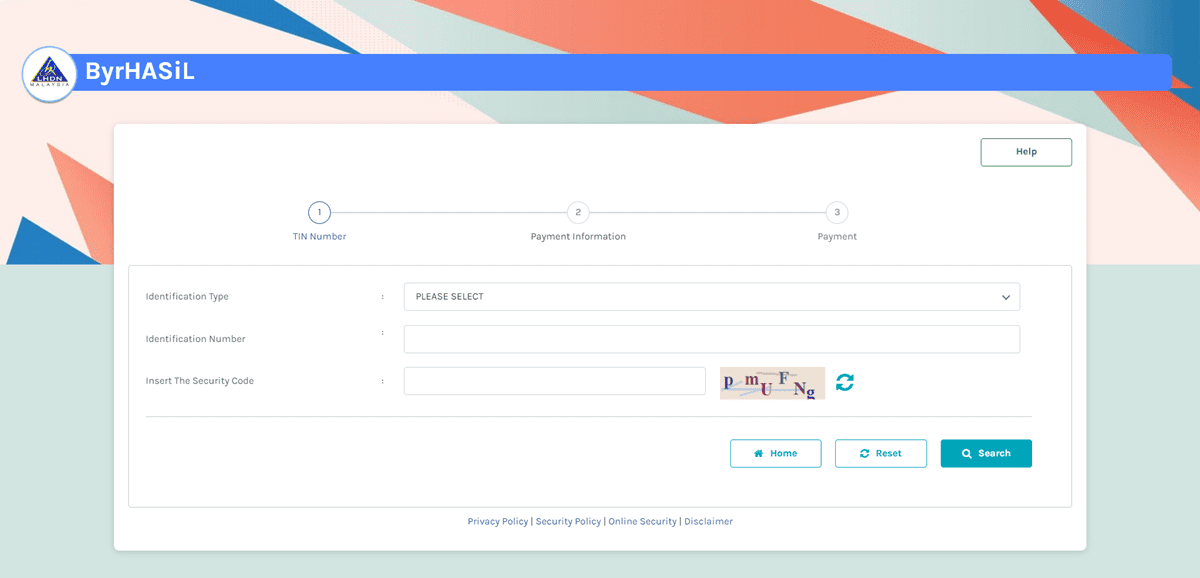

Payment methods include:

FPX via online banking

e-Billing through MyTax

Electronic Telegraphic Transfer for overseas taxpayers

Credit or debit card payments are accepted only at PPTH Kuala Lumpur.

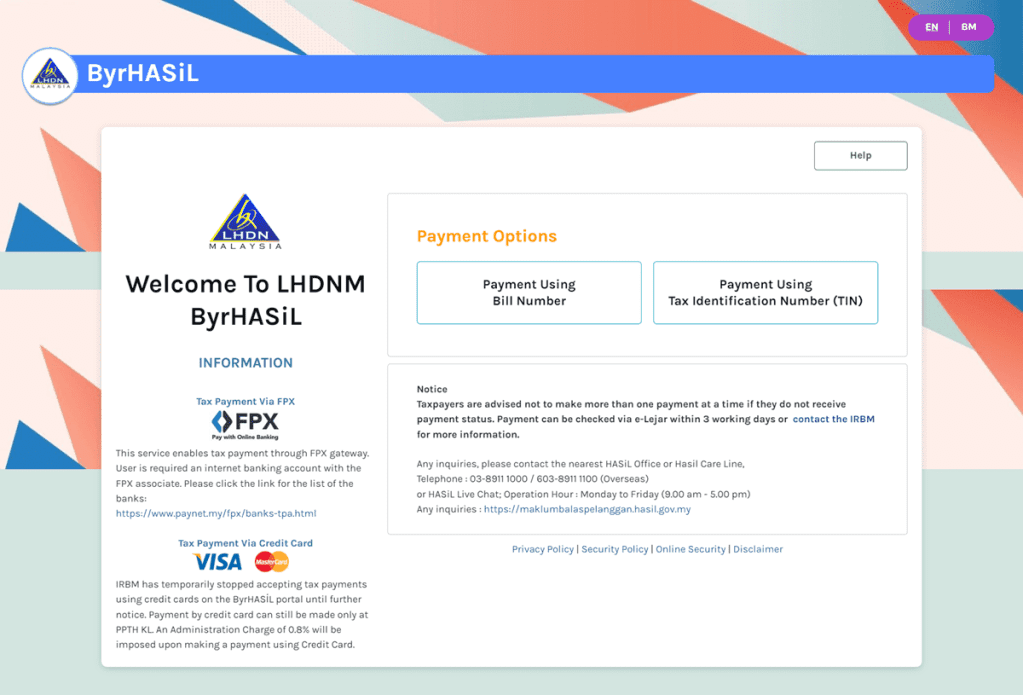

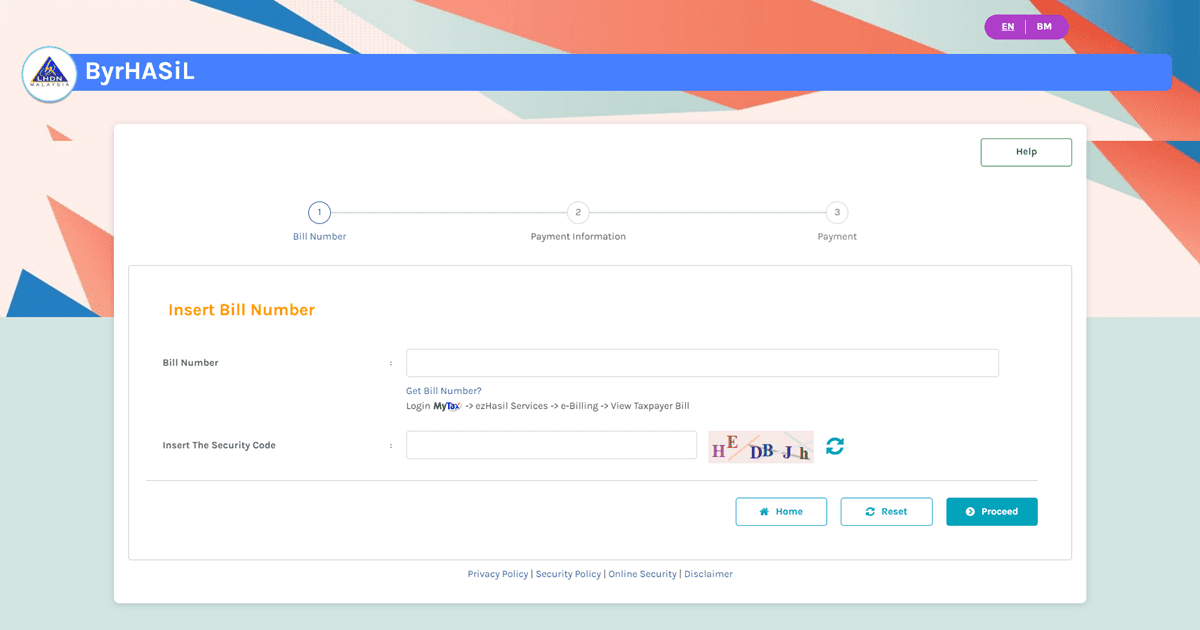

Bill Number Requirement

All tax payments must use a 16-digit bill number as a reference.

For e-Filing users, a bill number is automatically generated if tax is payable.

To retrieve your bill number:

Log in to MyTax

Navigate to “EzHasil Services” and select “e-Billing”

Overseas taxpayers using Electronic Telegraphic Transfer must generate a Virtual Account number.

Late Income Tax Payments

Failure to pay by the stipulated deadline will result in a 10% penalty.

If the outstanding amount remains unpaid after 60 days, an additional 5% penalty may be imposed.

Payment deadlines are:

15 May for individuals without business income

15 July for individuals with business income

The 10% penalty applies after the respective due date.

If you disagree with the penalty, you may submit a written appeal to the Collection Unit.

The penalty must be settled first. If your appeal is successful, LHDN will refund the amount.

Other Tax Offences and Penalties

Failure to file an Income Tax Return Form may result in:

A fine of between RM200 and RM20,000

Imprisonment for up to six months

Or both

Understating income may result in:

A fine of between RM1,000 and RM10,000

A penalty of up to 200 percent of the tax undercharged

Wilful tax evasion may result in:

A fine of between RM1,000 and RM20,000

Imprisonment for up to three years

A penalty of up to 300 percent of the tax undercharged

These penalties are imposed under the Income Tax Act 1967.

Appealing Your Notice of Assessment

After filing, LHDN may issue a Notice of Assessment detailing your taxable income and tax payable.

Review this document carefully.

If you disagree with the assessment, you may file an appeal within 30 days from the date of the notice.

To appeal:

Complete Form Q

Prepare a cover letter explaining the discrepancy

Attach supporting documents, including your ITRF

Submit them to the issuing LHDN branch

If you miss the 30-day deadline, you will need to apply for an extension of time using Form N, stating valid reasons such as medical treatment or absence from the country.

If the extension is granted, you must submit Form Q within 30 days from the issuance of Form CP15A.

Both Form Q and Form N are available on the LHDN website.

When You May Stop Filing Income Tax

In Malaysia, individuals are generally required to file an income tax return annually if they have an active tax file, even if their income is low or the tax payable is nil.

However, under certain circumstances, you may apply to close your tax file permanently.

According to LHDN’s guidelines, you may request closure if:

You have retired and no longer receive any taxable income

You are leaving Malaysia permanently

You are aged 55 or above and do not receive any taxable income

It is important to understand that tax file closure is not automatic. Simply having no income does not mean your filing obligation ends unless LHDN formally closes your file.

If you continue to receive income, including part-time, freelance, rental, or commission income, you are generally still required to file a tax return if your income exceeds the prescribed threshold. Filing serves as an official declaration of your income, even if no tax is ultimately payable.

For example, individuals below 55 years old who temporarily have no income may still need to file until their tax file is formally closed.

How to Close Your Tax File

To close your tax file permanently, you should:

Submit an official written request to the LHDN branch handling your tax file

State clearly the reason for closure, such as retirement or permanent departure

Ensure there are no outstanding taxes, penalties, or unresolved refunds

LHDN will review your request and notify you of the outcome.

If you are leaving Malaysia permanently, you should also apply for a Tax Clearance Letter before departure. This confirms that all tax matters have been settled and is particularly important for employees who cease employment in Malaysia.

Employers are required to notify LHDN of employee cessation, and final tax assessments may be issued before departure.

For more detailed procedures, refer to LHDN’s guidelines on cessation of employment and termination of service.

Important Reminder

Closing your tax file should only be done if you are certain you will no longer earn taxable income in Malaysia.

If you resume earning income after your tax file has been closed, you must reactivate or register again with LHDN to remain compliant.

*****

And that concludes our complete guide to filing personal income tax for 2026 (YA 2025), from understanding tax rates and reliefs to navigating amendments, payments, and appeals.

Filing your taxes may not be the most exciting annual task, but with proper preparation, the process can be straightforward and even financially beneficial. Whether you are aiming for a tax refund or ensuring you avoid penalties, staying organised and informed makes all the difference.

Set your reminders, keep your receipts, and file your tax return before the deadline. If you are ever unsure, consult a qualified tax professional to ensure everything is in order.

This guide is for general information purposes only and does not constitute tax advice. Taxpayers should refer to official LHDN publications or consult a licensed tax professional where necessary.

Follow us on our official WhatsApp channel for the latest money tips and updates.

Steffi Manisha Arokiam is a Tax Director at ThinkTX Consultants, where she leads the firm’s Transfer Pricing and e-Invoicing practice. She advises both individuals and corporations across a wide range of tax matters, including Real Property Gains Tax (RPGT), stamp duty, estate tax, and global mobility for expatriates. Recognised for combining strong technical expertise with a practical, solutions-driven approach, Steffi helps clients navigate complex tax issues with clarity and confidence.

A respected thought leader in taxation, Steffi has authored numerous technical articles and professional newsletters. Her work has been published by the International Bureau of Fiscal Documentation (IBFD) and Wolters Kluwer (CCH), and she has been featured on BFM 89.9 discussing crypto taxation.

Professional Affiliations

Member of the Malaysian Institute of Accountants (MIA)

Member of the Chartered Tax Institute of Malaysia (CTIM)

ASEAN Chartered Professional Accountant (ASEAN CPA)

Member of the International Fiscal Association (IFA)

Professional Trainer certified by HRD Corp

As a trusted tax partner of RinggitPlus, Steffi reviews and verifies all content relating to Malaysian taxation to ensure it is accurate, up to date, and practical — helping readers better understand the tax system and make the most of their tax position.

51vote

Article Rating

SHARE

About THE AUTHOR

Steffi Manisha Arokiam

Steffi Manisha Arokiam

Steffi Manisha Arokiam is a Tax Director at ThinkTX Consultants, where she leads the firm's Transfer Pricing and e-Invoicing practice. She advises both individuals and corporations across a wide range of tax matters, including Real Property Gains Tax (RPGT), stamp duty, estate tax, and global mobility for expatriates. Recognised for combining strong technical expertise with a practical, solutions-driven approach, Steffi helps clients navigate complex tax issues with clarity and confidence.

A respected thought leader in taxation, Steffi has authored numerous technical articles and professional newsletters. Her work has been published by the International Bureau of Fiscal Documentation (IBFD) and Wolters Kluwer (CCH), and she has been featured on BFM 89.9 discussing crypto taxation.

Professional Affiliations

Member of the Malaysian Institute of Accountants (MIA)

Member of the Chartered Tax Institute of Malaysia (CTIM)

ASEAN Chartered Professional Accountant (ASEAN CPA)

Member of the International Fiscal Association (IFA)

Professional Trainer certified by HRD Corp

As a trusted tax partner of RinggitPlus, Steffi reviews and verifies all content relating to Malaysian taxation to ensure it is accurate, up to date, and practical — helping readers better understand the tax system and make the most of their tax position.

Subscribe to our exclusive weekly newsletter and we’ll bring you the week’s highlights of financial news, expert tips, guides, and the latest credit card and e-wallet deals.

Thank you for subscribing!

Stay tuned for what’s to come next in the personal finance world

Comments (0)