Alex Cheong Pui Yin

Previously covered recruitment-related stories and had a short stint as a copywriter for the property industry. She subsequently developed an interest in investment and robo-advisors.

11th August 2020 - 4 min read

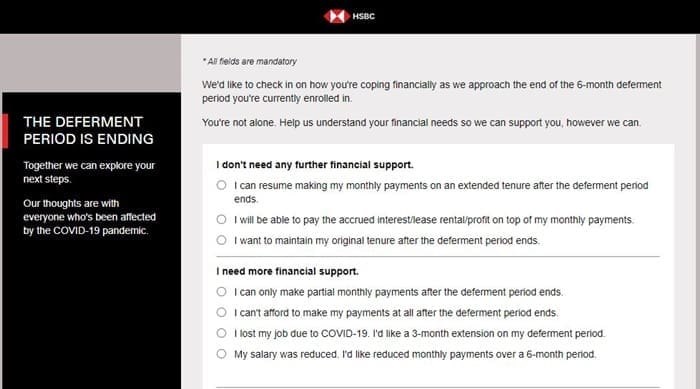

HSBC has updated its Covid-19 and moratorium support page with a contact form to assess its customers’ current financial position as the ongoing moratorium nears its end in September 2020. The form also doubles as the bank’s instrument to offer targeted post-moratorium aid to those who are truly in need.

Through the contact form, HSBC customers will be able to let the bank know if they are in need of further financial support after the moratorium is over. They are also invited to select the kind of assistance that they may need, such as:

The financial aids offered are applicable for the following facilities:

HSBC further said that it will get in touch with its customers to guide them on the next steps once bank personnel has reviewed the information submitted. As such, you can expect the aid offered to be tailored according to your needs and financial capabilities.

(Image: The Malaysian Reserve)

For clarification, HSBC’s updated FAQ has outlined the way its customers’ loan repayment schedule/amount will be affected once the moratorium is over. Here’s an idea of how things may change for you after September, according to the types of loans:

The tenure of your term loans and mortgages will be extended automatically by 6 months, and their terms and conditions will remain unchanged unless stated otherwise. Also, interest accrued on the principal outstanding balance during the moratorium will now be added to the outstanding amount of your loan.

Following this, customers who are ready to resume their loan/mortgage repayment can begin to do so in October. The instalment amount to be paid in October will remain the same as the sum paid pre-moratorium. The instalment amount for November onwards, however, will be revised to accommodate the addition of the accrued interest to your principal outstanding balance as well as any other rate changes. As a result, you will not need to repay a higher final amount at the maturity of your loan.

For overdrafts, the interest accrued during the April – September moratorium period will become due in October and must be repaid by then. Additionally, if you’ve exceeded the limit of your overdraft during the moratorium period, the overlimit must be repaid as a lump sum payment by October as well.

Your financing tenure will also be extended automatically by six months, with the terms and conditions of your financing remaining the same. Unlike conventional term loans and mortgages, however, the accrued profit will not be added to the principal outstanding balance of your loan.

In terms of your post-moratorium repayments, customers who are capable of repaying their loans can resume their monthly instalment payment in October. The monthly instalment amount for October will also remain the same as the amount paid pre-moratorium. It will then be adjusted in November onwards to accommodate any rate changes.

Note that the monthly instalments paid when you restart your loan repayment will be used to clear the profit/lease rental accrued over the moratorium period first. Only after the accumulated profit/lease rental has been cleared will your instalments contribute to repaying the remaining principal amount and its current profit/lease rental.

In this scenario, you may have to pay a higher final amount upon the maturity of your financing. The amount will depend on your outstanding amount, remaining tenure, and profit rate of your financing.

While you can stick to the repayment options outlined above, HSBC customers are also allowed to negotiate for other repayment alternatives to avoid a higher final amount at the maturity of their loan:

To speak to HSBC about these alternatives, you will have to fill in the bank’s dedicated contact form. You can also call the bank’s Collections Inbound teams at 03-2690 9999 (credit cards/financing) or 03-8894 1955 (mortgage) to make enquiries.

Find out more about HSBC’s post-moratorium financial support on its website.

Previously covered recruitment-related stories and had a short stint as a copywriter for the property industry. She subsequently developed an interest in investment and robo-advisors.

Subscribe to our exclusive weekly newsletter and we’ll bring you the week’s highlights of financial news, expert tips, guides, and the latest credit card and e-wallet deals.

Stay tuned for what’s to come next in the personal finance world

Comments (0)