How to prepare for a home loan

RinggitPlus

8th April 2013 - 3 min read

So you’ve done all your research on which banks offer the best home loans; read all the RinggitPlus guides to personal home loans; went through your accounts and expenses with a fine-tooth comb and decided that you are ready to be a home owner.

Congratulations, you have just made one of the biggest decisions of your life. Before you take that giant leap forward it might be worth your time to have a read through this article just in case you overlooked a few things. Nothing major but sometimes a little housekeeping goes a long way in making the loan application process a little less stressful.

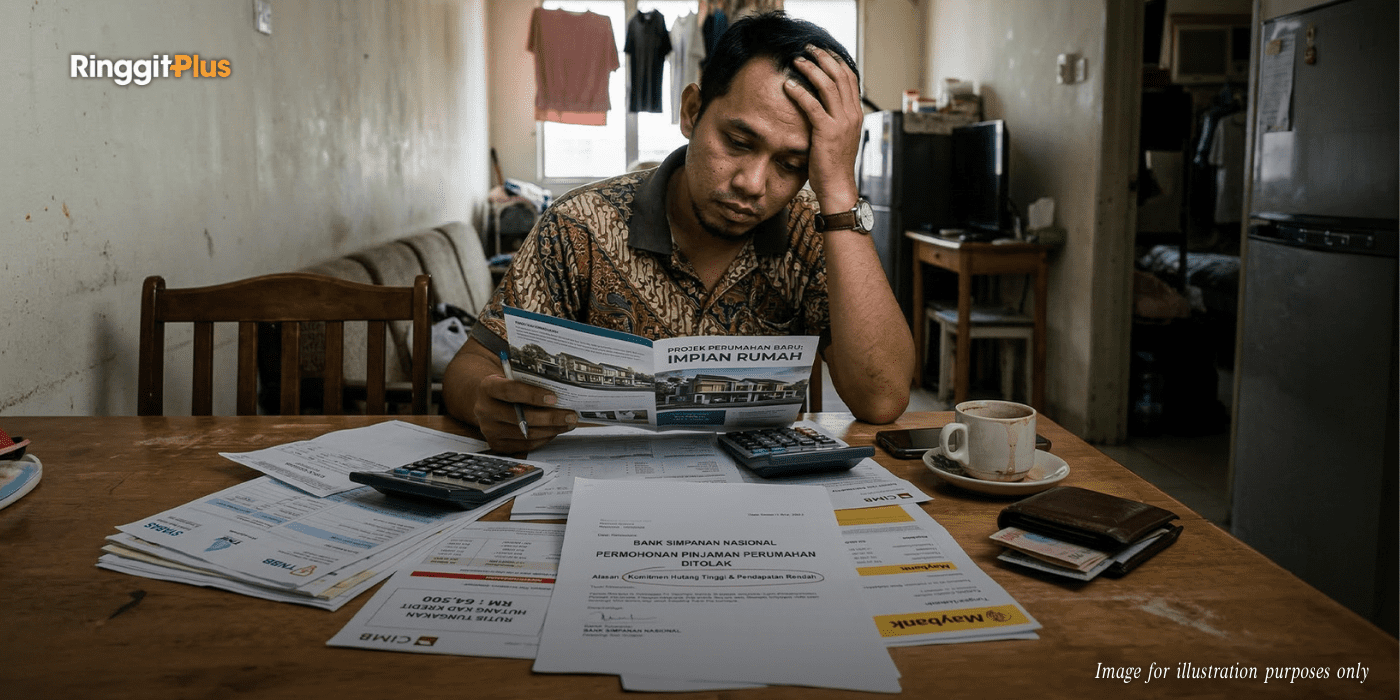

How much can you really afford?

There are three things you need to know before you even walk into a bank: margin, tenure and lock-in period. Yes, you’ve done your calculations and know how much you need to loan but sometimes things look different on paper than what it actually is.

Always have a Plan B. Ask the bank officer to play around with the numbers and consider all possible options. Also ask about the bank’s policy on early settlements and lock-in periods. Life is full of uncertainties and you might like to get ahead of your mortgage and retire early, for example. Even if it seems like an unlikely situation it’s always reassuring to know you have options.

It’s the small things that count

Remember you’re the customer and the bank is providing a service and profiting from it. If you’re not happy about the standards of their service and policies make it known and if nothing is done to rectify the issue, don’t hesitate to shop around for another bank. Other things to keep in mind:

· Administration fees and charges – Most competitive banks have done away with all these and as the customer you have the right to question your bank about all charges.

· Online facilities – Online banking in Malaysia is still in its infancy but some major names are leading the pack towards paperless transactions. Some banks allow you to submit your loan applications online and track its progress. The bolder ones will even promise to contact you in 48 hours. That’s how eager they are to do business with you!

· Ease of payment – How does your bank deal with your installments? Does it have 24-hour kiosks or online payments? It may sound trivial right now but this is something that you’re going to doing for a very long time on a monthly basis. Can you afford the time for over-the-counter transactions?

Documentations

Unfortunately the era of completely paperless transactions is still a faraway dream for us and you will be asked for copies of important documents. Some of documents commonly asked for include:

- Photocopies of your NRIC (or passport for non-residents)

- Income statements (3 or 6 months depending on the type of loan)

- Proof of your other existing loans (e.g. car loans)

- Personal details of your guarantor if your application requires one

- Booking receipt of your desired property

- Educational qualifications

- Latest EPF or LHDN statements

To minimise the hassle of your application process (and unnecessary charges) you might want to call up your bank and enquire about the type of documents they need. The more prepared you are, the less stressed out you will be if you need to make any adjustments in your financing later on.

Good luck!

About THE AUTHOR

RinggitPlus

Most Viewed Articles

Most Viewed Articles

Property

What is Cukai Tanah (Quit Rent)?

Have you paid your cukai tanah this year? Maybe you're not even sure what cukai tanah is? In that case, this is the article for you!

Property

Malaysia Bank Moratorium: Why You Should Opt For The 6-Month Deferment For ALL Loans (Updated)

EDITOR’S NOTE: This article refers to the 2020 loan moratorium, and the information here may be outdated. Please […]

Property

Malaysia Loan Moratorium 2021 Guide: Should You Take The 6-Month Deferment For Your Loans?

Under the PEMULIH stimulus package, Malaysia will once again see a 6-month moratorium for all loans, applicable to […]

Property

9 home loan rules you must read

You've read our handy guide on home loan basics - now check out these home loan tips to keep top of mind when you take out your first mortgage.

Comments (0)