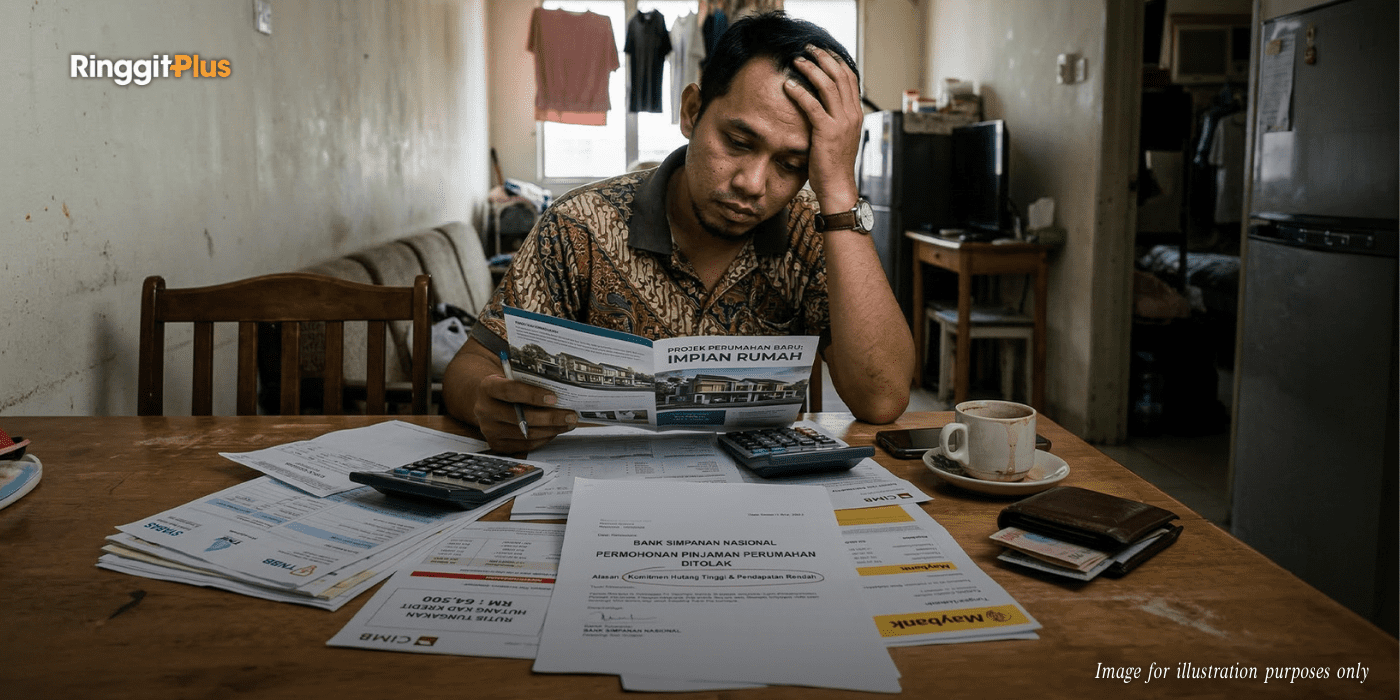

Trying to buy your first home usually begins with a simple question: will the bank approve the loan? According to property developers, that step is where many Malaysians are now getting stuck.

The Real Estate and Housing Developers’ Association Malaysia (Rehda) says more than two-thirds of prospective homebuyers fail to secure housing financing, largely because their income does not meet lending requirements or their existing debts are already too high.

The findings come from Rehda’s latest Property Industry Survey involving 166 developers nationwide. Around 72% of respondents reported that buyers faced financing difficulties, with most cases linked to banks rejecting mortgage applications after the purchase agreement stage.

Mortgage Rejections Are Blocking Property Transactions

Most property purchases in Malaysia follow a standard process. Buyers sign a sale and purchase agreement first, then apply for end-financing from a bank to complete the transaction.

End-financing refers to the mortgage loan that pays the developer the remaining purchase price. If the bank does not approve the loan, the buyer cannot proceed with the purchase.

Rehda president Datuk Ho Hon Sang said many loan applications fail because applicants already carry significant financial commitments. Outstanding credit card balances, personal loans, and car financing increase a borrower’s overall debt obligations and can push their debt service ratio beyond what banks consider manageable.

Banks also reject applications when income levels are insufficient to support the monthly instalments or when financial documentation submitted by buyers is incomplete.

In practical terms, a buyer may be able to afford the property price on paper but fail the bank’s affordability assessment once existing debts are taken into account.

Developers often encourage buyers to improve their financial profiles before applying for loans, Ho said. However, the final decision still depends on whether the borrower meets the bank’s lending criteria.

Middle-Income Buyers Are Also Struggling To Qualify

Financing difficulties are increasingly affecting buyers beyond the lower-income segment. Rehda’s survey shows that homes priced between RM500,001 and RM700,000 recorded the highest mortgage rejection rates, with between 31% and 45% of transactions failing to obtain financing.

This price range typically targets middle-income households, including dual-income families purchasing their first landed property or upgrading from smaller homes.

The trend reflects a mismatch between property prices and income growth. Research by Khazanah Research Institute previously found that households earning below RM3,000 per month account for about 15% of Malaysia’s population, yet only around 3% of newly launched homes are considered affordable for this income group.

Even though roughly half of new housing launches are priced below RM300,000, those properties remain beyond the financial reach of many households whose incomes are low or unstable.

Debt Levels And Income Gaps Are Driving Loan Rejections

Banks assess housing loan applications primarily based on repayment ability rather than property price alone.

Lenders evaluate a borrower’s debt service ratio, which measures how much of monthly income is already committed to debt repayments. Existing obligations such as credit cards, personal loans, and vehicle financing all contribute to this calculation.

If the ratio exceeds the bank’s acceptable threshold, the mortgage application may be rejected even if the buyer has already paid a booking fee or signed a purchase agreement.

Rehda immediate past president Datuk NK Tong said the widening gap between income growth and property prices remains the underlying driver of financing difficulties.

He suggested that banks could consider allocating part of their mortgage portfolios specifically to affordable housing loans, proposing that around 30% of lending could be directed toward this segment. Such an approach, he argued, could encourage banks to work more actively with borrowers who genuinely need assistance.

The suggestion remains a proposal rather than a policy change, and banks are currently not required to allocate a specific share of mortgage lending to affordable housing.

Tighter Financing Is Also Affecting Developers

Financing conditions are also becoming more stringent for property developers.

Developers rely on bridging financing, which refers to short-term loans used to fund construction while projects are being built and sold. According to Rehda, banks have become more cautious in providing this financing.

Some lenders now require developers to achieve sales thresholds of between 30% and 60% before releasing funds. Banks are also requesting additional documentation and imposing stricter conditions before allowing developers to draw down financing.

These requirements increase the financial risk of launching new projects and may lead developers to delay construction until sufficient buyer commitments are secured.

Unsold Homes Continue To Build Up

At the same time, unsold completed housing units are increasing across the country.

About 60% of developers surveyed reported having unsold completed residential properties as of the end of 2025. Loan rejections, weak demand, and high property prices were identified as the main reasons buyers were unable to complete their purchases.

Nearly half of the unsold units are priced below RM500,000, indicating that affordability challenges extend into what is often considered the mid-market segment.

Two- to three-storey terrace houses account for the largest share of unsold units at 26%, followed by serviced residences at 19% and single-storey terrace houses at 18%.

Ho noted that sales performance still depends heavily on location and the specific market where a project is launched. Properties in certain areas continue to sell steadily, while others face slower demand due to local income levels and supply conditions.

Financing Constraints Are Likely To Remain A Key Barrier

The survey highlights a persistent gap between housing supply, household income, and bank lending standards.

Developers may continue to launch new projects and buyers may still want to purchase homes, but the transaction only proceeds when banks are confident that borrowers can comfortably repay the loan.

Over the next one to three years, this financing constraint is likely to remain a major friction point in Malaysia’s housing market. Unless household incomes rise more quickly, property prices adjust, or lending structures change, many buyers will continue to encounter the same obstacle at the final stage of the purchase process: securing mortgage approval.

Follow us on our official WhatsApp channel for the latest money tips and updates.

Samuel writes about personal finance and financial news, focusing on how banking updates, policies, and promotions affect everyday money decisions. He enjoys making complicated financial topics easier to follow. Outside of writing, he spends his time watching TV shows and occasionally convincing himself he will only watch one episode.

00votes

Article Rating

SHARE

About THE AUTHOR

Samuel Chua

Samuel Chua

Samuel writes about personal finance and financial news, focusing on how banking updates, policies, and promotions affect everyday money decisions. He enjoys making complicated financial topics easier to follow. Outside of writing, he spends his time watching TV shows and occasionally convincing himself he will only watch one episode.

Subscribe to our exclusive weekly newsletter and we’ll bring you the week’s highlights of financial news, expert tips, guides, and the latest credit card and e-wallet deals.

Thank you for subscribing!

Stay tuned for what’s to come next in the personal finance world

Comments (0)