How To File Your Taxes If You Changed Or Lost Your Job Last Year

RinggitPlus

3rd April 2024 - 6 min read

It is not an overstatement to say that the past few years have been difficult for many people, with Covid-19 having wreaked havoc across the world. While Malaysia has slowly begun to recover from the far-reaching economic impact of the pandemic – which affected many business across different industries – some people have still had to find new jobs with another employer or become unemployed in the past year.

With the tax season now upon us, some frequently asked questions by these groups of people are these: what does the tax-filing process look like now? Will they need to take additional steps or fill in extra forms? Do jobless individuals still need to file their taxes if their total income for 2023 fall beneath the requisite amount of RM34,000?

We’ll discuss these and more in this article.

If you changed jobs in the previous year

The tax-filing process for someone who changed jobs in the previous year isn’t too different from the usual procedure, actually! It will involve some extra calculations and EA forms, but otherwise, everything else is pretty much the same.

Similar process, but with extra EA forms

Essentially, filing your taxes when you have more than one employer in the assessment year means you’ll need to combine the total income earned from both companies in a single BE form. The most efficient way to do this is with the EA forms obtained from your previous and current employers. Note that all employers are legally bound to provide their employees – both current and former – with an EA form, so make sure to collect yours!

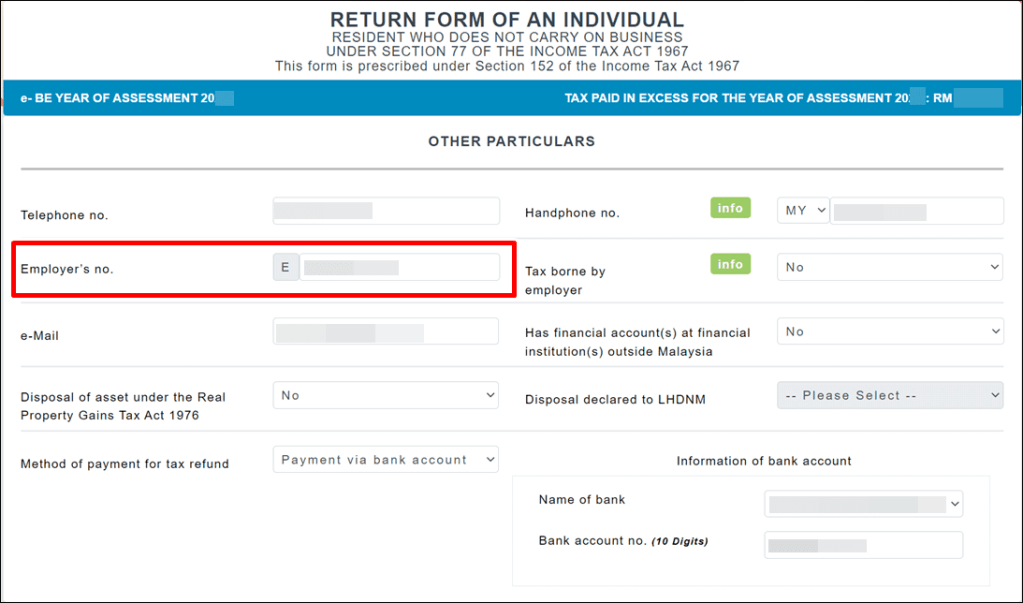

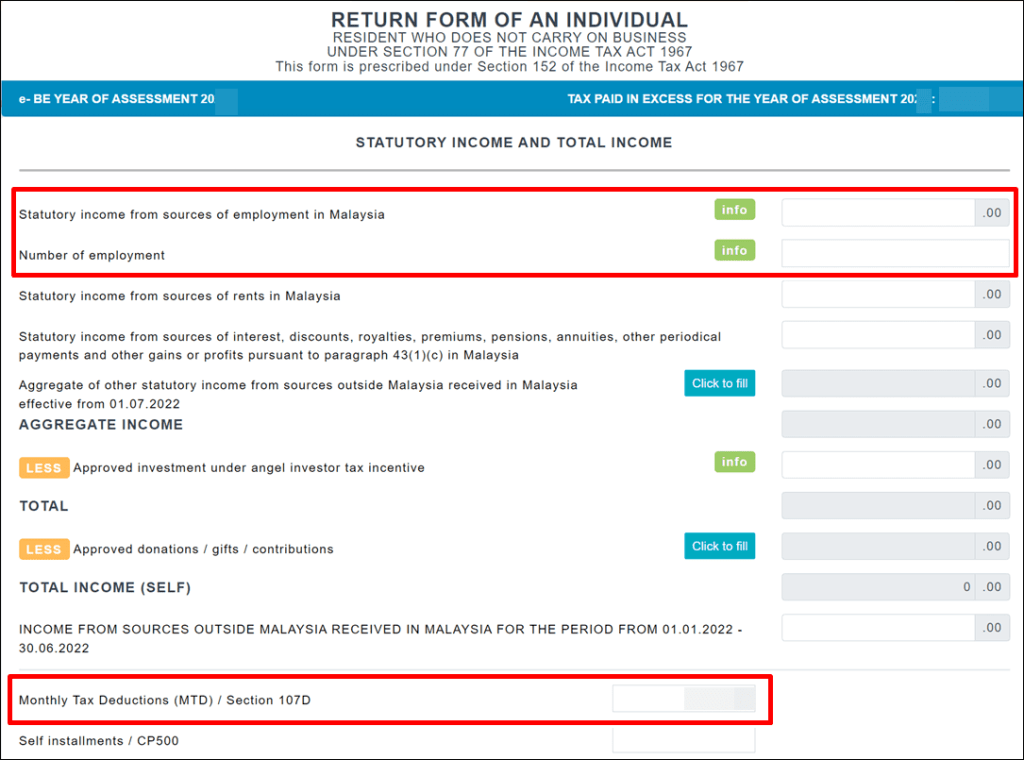

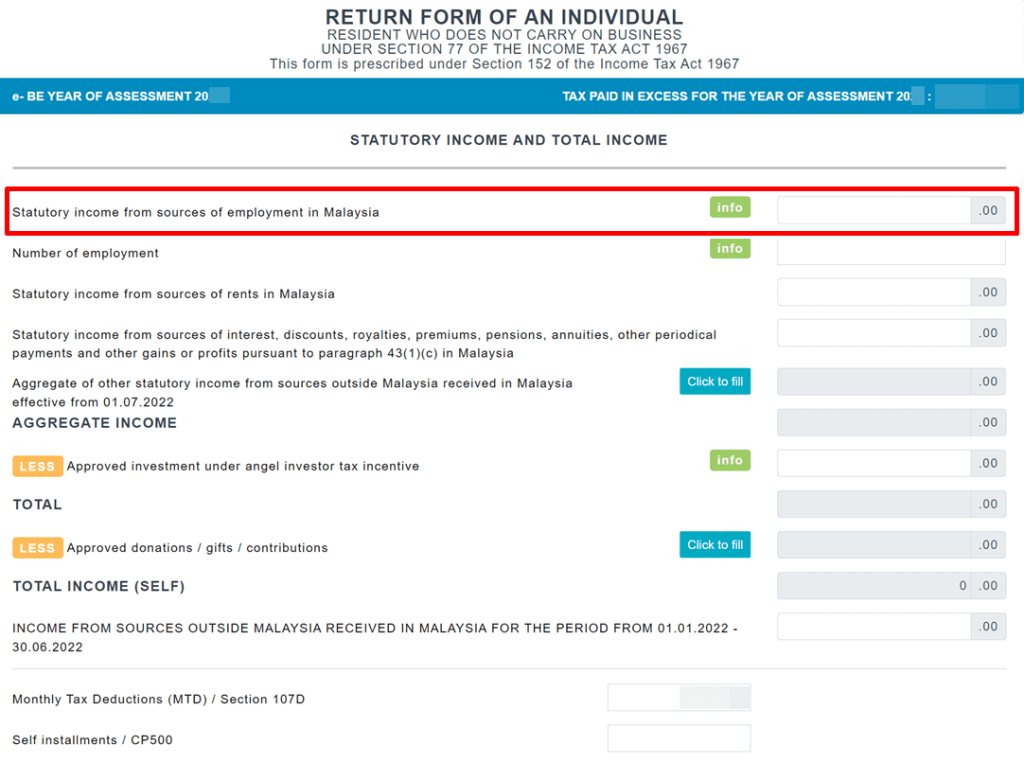

Your EA forms will provide a summary of the information that you need to file your taxes seamlessly: total income, Employees’ Provident Fund (EPF) contribution, Social Security Organisation (SOCSO) contribution, as well as monthly tax deduction. When filing up your BE form, just add the total amount of the respective categories from the different EA forms, and you’re good to go! Be sure to also update your employer’s tax number (E Number) so that it reflects your current employer’s.

What if you didn’t get your EA form from your previous employer?

You can still file your taxes, but it’ll just take a bit more work on your end. Not having your EA form from your previous employer means you’ll need to find all the required information yourself via your salary slips, EPF, and SOCSO statements from the year of assessment. Clearly, this will involve some tedious work, and there is always the likelihood of miscalculations, so do your best to follow up with previous employers before resorting to manual calculations!

If you really are left with no choice, however, your total income, EPF and SOCSO contributions, as well as your monthly tax deductions (MTD/PCB) can be found in your salary slips. Collect all your salary slips from the different employers that you’ve worked with in the year of assessment, and compile these figures. Naturally, this gets more cumbersome the more companies you’ve worked with, so be extra cautious here!

You can also cross check your EPF contributions through your EPF statement online, as well as your SOCSO contributions via your iPERKESO account.

If you were retrenched or unemployed in the previous year

As a rule of thumb, any individuals earning a minimum of RM34,000 after EPF deductions must file their taxes. But what if you were retrenched or unemployed during the year of assessment, and your income did not come up to the requisite amount? Will you still need to file your taxes?

The answer: Yes. You are obligated to file your taxes yearly once you’ve registered your tax file, even if you do not earn the requisite amount. It is also necessary to file your taxes as your retrenchment or unemployment compensations are considered as taxable income – with some eligible for tax exemptions.

Compensation for loss of employment

According to the Lembaga Hasil Dalam Negeri Malaysia (LHDN), compensation for the loss of employment is defined as a payment that is made by employers to their employees upon their termination. Examples of compensation for loss of employment include:

- Salary or wages in lieu of notice

- Compensation for breach of a contract of service

- Payments to obtain release from a contingent liability under a contract of service

- Ex-gratia or contractual payments, such as redundancy or severance payments (such as Voluntary Separation Schemes (VSS))

- Payment to restrict an employee from finding similar types of employment after termination with current employer

LHDN further noted that a portion of these compensations are exempted from tax under the Income Tax Act 1967. More specifically, the compensation is exempted as per the following circumstances:

- Full exemption: The compensation is made on account of loss of employment due to ill health

- Partial exemption: Exemption of RM10,000 for every completed year of service (full 12 months) with the same employer or with companies in the same group

Filing your taxes as an unemployed individual

The tax-filing process for an unemployed individual is not too different from the usual process either! You’ll have to include the compensation amount as part of the statutory income from your employment, along with your other earnings, but make sure to deduct the allowed exemption before doing so. Other than that, you can go ahead and fill in your BE form as usual.

For precaution, make sure to compile and keep all the necessary documents to prove that the lump-sum payment that you receive is your compensation for loss of employment. Aside from your termination letter and contract, you may also want to save your payslips and EA forms as evidence of your tenure with your former employer.

***

With this, we hope that you have a better idea as to how to file your taxes under these different circumstances. Do also check out our Income Tax page for other tax-related content, such as our step-by-step YA2022 Income Tax Guide, tax reliefs that you can tap into, and how to file your taxes if you’re a first-timer.

About THE AUTHOR

RinggitPlus

Most Viewed Articles

Most Viewed Articles

Tax

LHDN Wants You To Start Collecting e-Invoices for Tax Relief

The Inland Revenue Board (LHDN) is urging taxpayers to request e-invoices for every purchase tied to individual tax […]

Tax

How To Tell Lifestyle Relief From Sports Relief

From the Year of Assessment 2024 onwards, LHDN moved sports equipment and gym memberships out of the general […]

Tax

Government Refunds RM14.7 Billion In Excess Tax Payments

The government has refunded RM14.7 billion in excess tax payments covering 3.17 million taxpayer cases as of 30 […]

Tax

Your Course Fees Can Fall Under Two Tax Reliefs

Where you claim your course fees can change your tax bill by a few hundred ringgit. The same […]

Comments (29)

Just came across this article after submission of 2025 tax. How do I now submit for tax exempt amount for compensation of loss of employment paid by my previous employer?

Thank you for your question!

You can still make corrections or updates by filing an amendment through the e-Filing system (look for the “Amendment” option under your BE form). Alternatively, you can reach out directly to Lembaga Hasil Dalam Negeri Malaysia (LHDN) with the relevant supporting documents such as your termination or compensation letter, EA form, and proof of payment. LHDN will review your submission and make the necessary adjustments if the exemption applies.

Do note that this is general information only and should not be treated as professional tax advice. Please refer to LHDN for case-specific confirmation.

If I have stop working and no income for Year 2024, can my spouse file his tax with the type = ‘Self : Individual is Single / Widow / Widower / Divorcee / Spouse with no source of Income’

Do I still need to file my tax with 0 income ? If he choose the type = 4 ?

If you had no income in 2024, yes, your spouse can select the filing type “Self: Individual is Single / Widow / Widower / Divorcee / Spouse with no source of Income” when submitting his tax return. As for you, technically, if you had absolutely zero income in 2024 and no tax was deducted (e.g. from investments or other sources), you’re not required to file a tax return. But if you already have a tax file with LHDN, it’s a good idea to log in and submit a ‘NIL’ return just to keep things in order and avoid any reminders… Read more »

My previous employer suddenly liquidated, so I was unemployed starting from January last year. But the employer compensated me in the same year after they liquidated. And I’m temporarily working as a freelancer ever since, without registering a company. In this case, what employer tax number should I fill in?

If that’s the case, you don’t need to worry about filling in their tax number. For your freelance work, since you’re not registered as a company, you can leave that section blank or just put “Self-Employed” when asked for your employer’s tax number.

Want to ask, I changed job last year. It’s higher pay. So when I plus both EA form and fill up my tax, including filling up the rebate items such as lifestyle and others, I end up needing to pay more for tax (few thousand). Is this a normal scenario? Because I heard when you change job, it’s likely you pay for tax instead of getting money / rebate for it.

It’s common to pay more tax when switching to a higher-paying job. Each employer might have taxed you separately, not considering your total yearly income. When filing taxes, LHDN calculates based on your total income, so if previous deductions weren’t sufficient, you may owe more. Higher income often leads to higher taxes, even with rebates.

What if I have resigned during April and only had a job on July until October? How should I fill the form? I’m kind of lost on this part.

Same process – you need to tally up all incomes from your different employers.

If I resign from the company to continue my studies, do we need to do e-filling for the periods that we studies?

Because we no longer working and didn’t have any company release EA form to us.

Following this query! Please provide a feedback for us.

I’m querying a similar case – from a salary that is qualified to pay tax to a salary that doesn’t, from the article it says “You are obligated to file your taxes yearly once you’ve registered your tax file, even if you do not earn the requisite amount.”.

Even if we file a non-requisite amount, is there any amount to be paid?

I assume you just have to quickly fill in the forms with 0s then call it a day. It is stupid but yeah.

I left the company in Oct’2022 due to company’s ongoing court case liquidator process and my employment contract not renew.

In 2023 not working anymore.

Current my ex- employer human resource not exist anymore. Do not know my ex- employer notify LHDN. How do I notify LHDN that I am not working and no income.

Please advise.

You can inform LHDN directly by submitting a letter or form stating that you are no longer employed and have no income. Include your personal details and relevant documentation such as your resignation letter or termination notice. Contact LHDN for specific instructions on how to proceed.

This article does not Illustrate with clarity How to fill BE form for job loss compensation. There are many enquiries posted…

My brother was asked to resign and company paid him RM40k+. Income tax deduction is RM7688.10

while i was helping him to e-filing , it shows the only amount that is overpaid is RM393.25 in Y2021.

My brother is currently jobless and does not have any income. Will LHDN return the remaining sum when we do e-filing for Y2022?

Hello,

May I know which column in BE form can I put the amount of the retrenchment money I received from my previous employer, and which column can I put in the compensation year (e.g. RM20,000 x years of service) so that it will be deducted as tax exemption?

Thank you for you help.

Appreciate if someone can enlighten this issue

The amount of retrenchment received is included in the “statutory income of employment”.

The computation will be like:

Amount of compensation a

Less: Amount exempted (RM20,000 x years of completed service) (b)

= Taxable compensation c

If the Amount exempted > Amount of compensation, then Taxable compensation would be 0.

So, C will be included as part of B1 Statutory income from employment.

Hope this is clear and do correct me if it is wrong.

I have done my tax clearance in early Jan 2022 due to a retrenchment. Am I still required to do my tax filing for YA2021?

I was retrench after serving 10 years for the company last year. does this mean I’ll be able to get 200K of tax exemption for lost of employment in 2021. Could you pls share the link to the said increased by the government. thanks

In 2021 within a year, I resigned from one job and joined another job and resigned again (not working until now). How to do file my tax? Thank you in advance.

I was retrenched in Dec 2020. and already got my surat penyelesaian cukai from lhdn.

From Jan 2021 until Dec 2021 I worked for a friend who is doing a small kampung business.

He pays me monthly but there is no proper record, there is also no epf, socso.

Do I have to declare the income received?

If I have no compensations and no income in the past year, do I still need to submit Tex filing?

Yup, you do. you just need to declare zero income for YA 2021.

the answer i need the most… thanks for sharing

I applied iLestari last year do I have to put the amount received throughout last year in Statutory Income from interest,other periodical payment etc?

Thank you in advance.

No, i-Lestari are withdrawals from your income in the past.