Every year, millions of Malaysians make the same promise on New Year’s Day: save RM500 a month, pay off credit card debt, and finally start that emergency fund. By February, that RM500 has been “borrowed” to cover car repairs or a colleague’s wedding. Sound familiar?

The problem isn’t that you lack discipline. Willpower is a limited resource that gets depleted by the dozens of financial decisions you make every day. Coffee or tea? Grab or drive? That sale at Shopee ends tonight. By the time payday arrives, your decision-making battery is already flat.

The answer? Build a system that removes decisions entirely.

Pay Yourself First With The Toll Booth Method

The idea behind automation is simple: make every important financial decision once, then let your bank do the work for the next 12 months. Most of us operate with one account where salary comes in, and spending goes out, hoping there’s something left over. That rarely works. An automated system flips this around. Money gets moved to savings and bills get paid the moment your salary hits, before you have a chance to spend it.

Think of your savings like a toll booth on the highway. Before your money reaches your spending wallet, it has to pay the toll first.

The traditional approach looks like this: earn RM5,000, spend throughout the month, save whatever’s left (usually nothing). The toll booth method looks different: earn RM5,000, automatically move RM500 to savings, pay bills, and spend the rest.

The transfer happens on payday itself, or the morning after — automatically, without your input.

Here’s how the money should flow:

Step 1: Salary hits your main account.

Step 2: Automated transfer moves a fixed amount to your savings immediately.

Step 3: Automated payments handle your loans, utilities, and credit card bills.

Step 4: Whatever remains is your guilt-free spending money.

Instead of spending and hoping to save, you save first and spend what’s genuinely available.

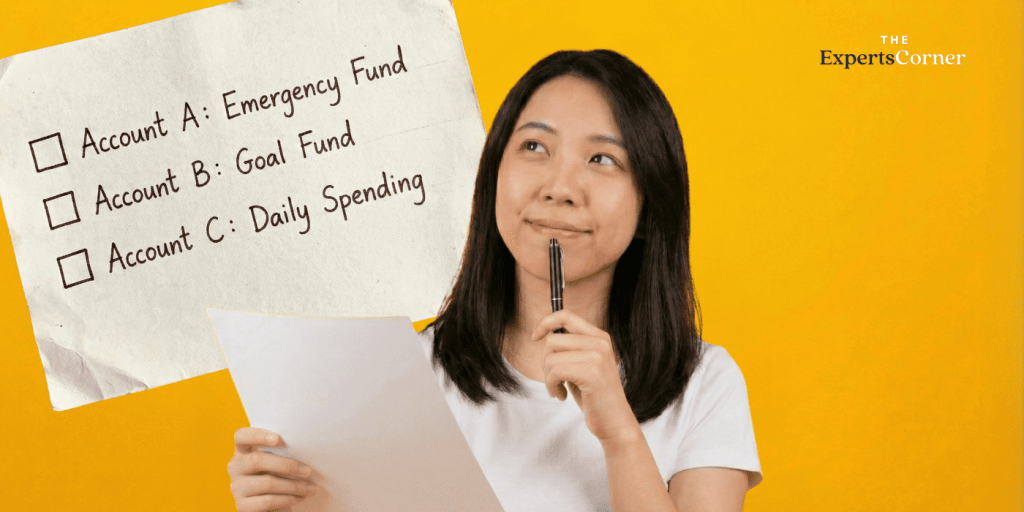

Three Accounts, Three Jobs

One big bank account where everything lives together is a recipe for financial confusion. When your emergency fund, holiday savings, and grocery money all sit in the same pool, it’s impossible to know what you can actually spend.

Separating your money into distinct accounts tricks your brain. You’re less likely to raid your emergency fund for a spontaneous weekend trip when it’s clearly labelled and sitting elsewhere.

Your emergency fund: This is three to six months of expenses, untouched unless there’s an actual emergency. Job loss counts. A flash sale on electronics does not.

Your goal savings: The Bali trip next year, the laptop you’ve been eyeing, that house down payment you’re working toward. Each goal can be a separate sub-account or a single pool you track mentally.

Your spending money: Groceries, petrol, dining out, Grab rides, and that monthly Spotify subscription. This is what you actually live on.

For your emergency fund, consider a high-yield savings account that beats inflation, with rates between 3%-4%. Even a basic savings account offers some return, and high-yield options can add RM200 to RM400 per year on a RM10,000 balance, depending on rates and conditions.

For goal savings, many digital banks now offer goal-based features. Touch ‘n Go GOinvest, GXBank’s savings pockets, Ryt Bank’s Pocket, and Boost let you create separate “pots” within one app. The promotional interest rates are similar to high-yield savings accounts at 3%-4%, and the psychological separation helps you avoid dipping into holiday funds for everyday expenses.

Setting Up Your Automated Flow

The magic happens through “Standing Instructions” or automated transfers. Every Malaysian bank offers this, though they call it different things.

Log in to your online banking. Look for “Standing Instruction,” “Recurring Transfer,” or “Scheduled Payment.” Set the transfer date for the day after your typical payday. Schedule transfers to your emergency fund and goal savings accounts. Set auto-payment for your credit card minimum (or full balance, ideally) and any loan instalments. The whole setup takes about twenty minutes.

A practical example: Sarah earns RM4,500 per month, paid on the 28th. On the 29th, her bank automatically transfers RM300 to her emergency fund and RM200 to her travel savings. Her credit card bill and car loan get auto-deducted. What lands in her spending account is around RM2,800, and that’s what she lives on.

Making The System Work Harder

Once your basic flow is running, you can optimise the tools you’re using.

For everyday spending, a cashback credit card turns mandatory expenses into small refunds. Fill up petrol, buy groceries, pay your phone bill, and earn 1% to 8% back depending on the card and category.

Just make sure the card matches what you actually spend on. A petrol-focused card is pointless if you take the LRT to work. A grocery card makes sense if you’re doing the family shop weekly. Not sure which card suits your spending? Use our comparison tool to filter by your main spending categories.

Your emergency fund protects against short-term problems, but a medical crisis can wipe out years of savings in a single hospital stay. If you don’t have medical coverage through your employer, review whether your personal medical card provides adequate coverage. A RM50,000 annual limit might sound like a lot until you see the bill for a private hospital admission.

What Changes When You Automate

This system removes the daily mental burden of financial decisions.

When your automation is running, you stop having the internal debate every time you see something you want to buy. The money in your spending account is genuinely available. Spend it. Enjoy it. Your bills are paid, your emergency fund is growing, and your goals are getting funded, all without you thinking about it.

You just need twenty minutes to set up your system, and watch your money take care of itself.

Follow us on our official WhatsApp channel for the latest money tips and updates.

As a creative content writer, Eloise has covered finance, business, lifestyle topics, and even moonlights as a singer-songwriter outside of RinggitPlus. Her current interests are learning the best ways to optimise spending and credit card hacks to gain more airline miles.

00votes

Article Rating

SHARE

About THE AUTHOR

Eloise Lau

Eloise Lau

As a creative content writer, Eloise has covered finance, business, lifestyle topics, and even moonlights as a singer-songwriter outside of RinggitPlus. Her current interests are learning the best ways to optimise spending and credit card hacks to gain more airline miles.

Subscribe to our exclusive weekly newsletter and we’ll bring you the week’s highlights of financial news, expert tips, guides, and the latest credit card and e-wallet deals.

Thank you for subscribing!

Stay tuned for what’s to come next in the personal finance world

Comments (0)