Malaysia Personal Income Tax Guide 2017

RinggitPlus

13th April 2017 - 7 min read

It’s income tax season once again! There is still some time to file your yearly income tax and this is the guide you need to get through your filing. We’ll try our best to cover all the necessary bases when it comes to taxes so you can file and pay yours in a timely manner while saving money at the same time. Let’s get started!

Tax Rates

First things first, you need to know your tax rates. It’s always a percentage of your chargeable income (more on that later). The more you earn, the higher the percentage of tax you need to pay. However, that higher percentage is only applied to the amount that’s higher. So you never end up with less net income after tax even if you earn more.

Let’s look at the tax rates for the Year of Assessment 2016 and see how much you need to pay:

You will notice that the final figures on that table are in bold. That’s because the rates for people who earn on that last two higher brackets have been increased from 25% to 26% and 25% to 28%. If you didn’t earn that much last year, you probably don’t need to worry about that.

It’s important to note also that the table above only applies to resident individuals who make their income in Malaysia. Not sure if that’s you? Well, if you are:

- in Malaysia at least 182 days of the year,

- in Malaysia for less than a consecutive 182 days, but the gaps in between those days were spent away on business trips, medical treatment, or social visits (of less than 14 days),

- in Malaysia for 90 days or more during the year and in any 3 of the 4 previous years,

…then you’re a tax resident. So the rates on the table above would apply to you.

But if you’re non-resident individual earning income in Malaysia, your tax rates are different. It looks more like this:

Some items in bold for the above table deserve special mention. Technical or management service fees are only liable to tax if the services are rendered in Malaysia. While the 28% tax rate for non-residents is a 3% increase from the previous year’s 25%.

No guide to income tax will be complete without a list of tax reliefs. The below reliefs are what you need to subtract from your income to determine your chargeable income.

Chargeable Income

Your chargeable income is best illustrated with an example like so:

Say you are earning a RM40,000 per year salary, you have a RM2,000 local bank interest income as well as RM13,000 from property rental income a year. That’s an annual income of RM55,000.

Let’s take into account the standard RM9,000 individual tax relief as well as a maximum relief of RM6,000 for EPF contributions.

Assume your EPF contribution is calculated at 11% of RM40,000. That gives you RM4,400, which is still under RM6,000, meaning your EPF earnings are completely exempted.

All local bank interest income is still tax exempted, so that RM2,000 local bank interest income doesn’t count either.

By applying these exemptions and reliefs, your chargeable income will actually be:

RM55,000 – RM2,000 – (RM 9,000 + RM4,400) = RM39,600. A much lower figure than you initially thought it would be.

Of course, these exemptions mentioned in the example are not the only ones. Which is why we’ve included a full list of exemptions for the year assessment of 2016 here for your calculation:

Tax Reliefs for Year of Assessment 2016

Now that you have your reliefs and you have your tax rates, you’re ready to calculate your chargeable income right? Not quite. Because there might be forms of income which count towards your chargeable income but is separate from your salary. By which we mean perquisites and benefits-in-kind.

Perquisites

Also referred to as company or employee perks, these items have cash value and are counted as part of your income. Perks include gift vouchers, company credit cards, company insurance premiums, staff discounts, or any other kind of sponsored payment made by the company on your behalf.

A rule of thumb to determine whether or not something is a perk is to think about whether or not you would have to pay (or pay more) for it if you weren’t working for the company. If the answer is yes, that’s a part of your income, and is taxable.

Thankfully, some perquisites are tax exempted by certain amounts:

Another entry in bold for this table refers to the special conditions of the taxable value of travel allowances. If you travel as a heavy part of your work and the company gives you allowance, it’s only exempted up to RM6,000. However, your expenses towards the travel used for work can be deducted from your gross income, provided you keep a record of these expenses.

Benefits-in-Kind

These also count towards part of your income. Think of these as perks, but ones that cannot be directly converted to cash. There are two ways to determine the monetary (thus taxable) value of these benefits:

The Formula Method, which uses this calculation:

Value of asset / Lifespan of asset = Annual value of benefit

and the Prescribed Value Method, which assigns a predetermined value from a list sorted by classification of asset.

We recommend sticking to the formula method for most benefits-in-kind since the prescribed value method isn’t really available for all asset classifications. However, we’ve provided the list of prescribed values here anyway so you can decide for yourself whichever is cheaper for you.

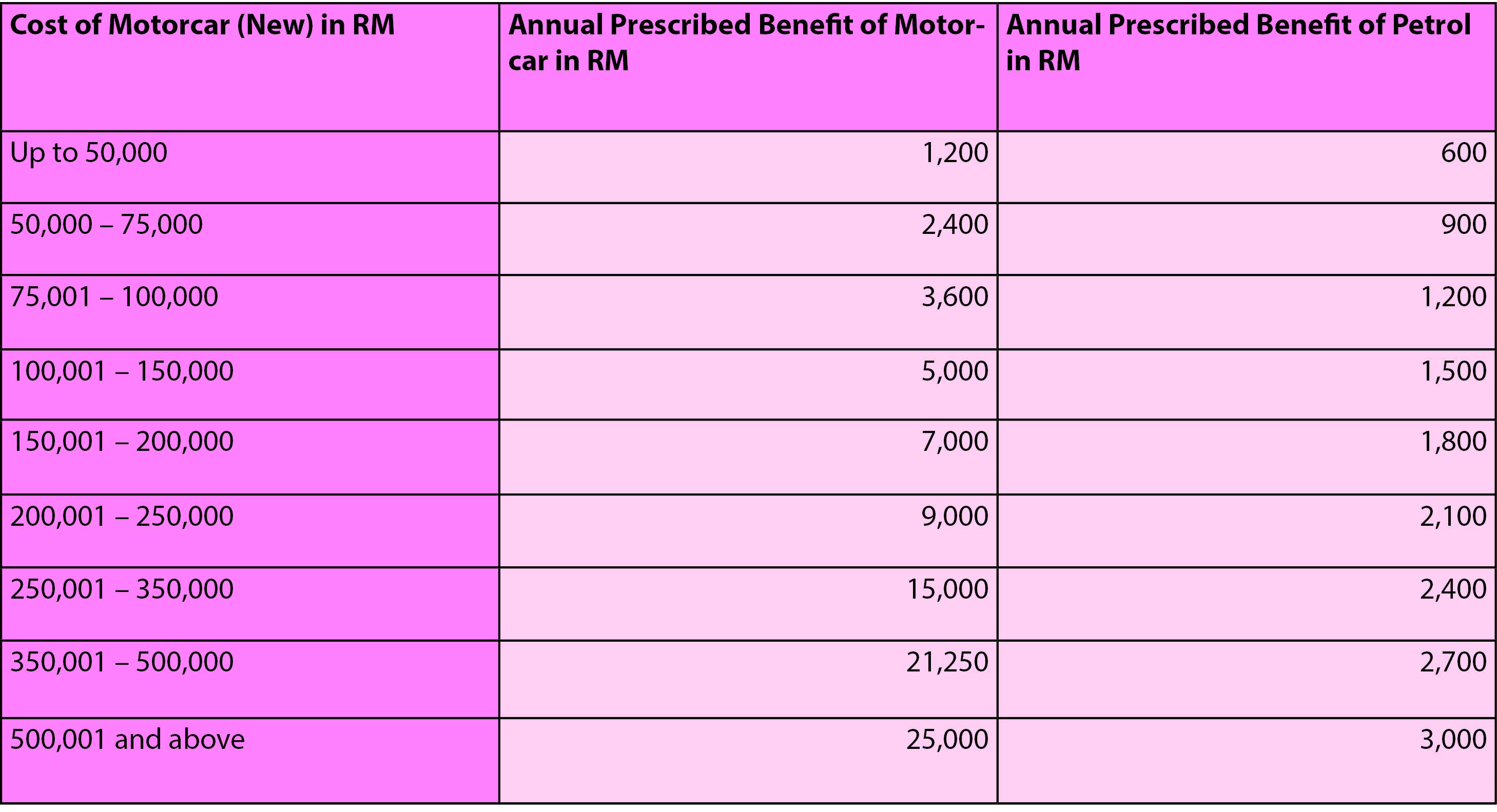

Prescribed Value of Motorcars and Related Benefits

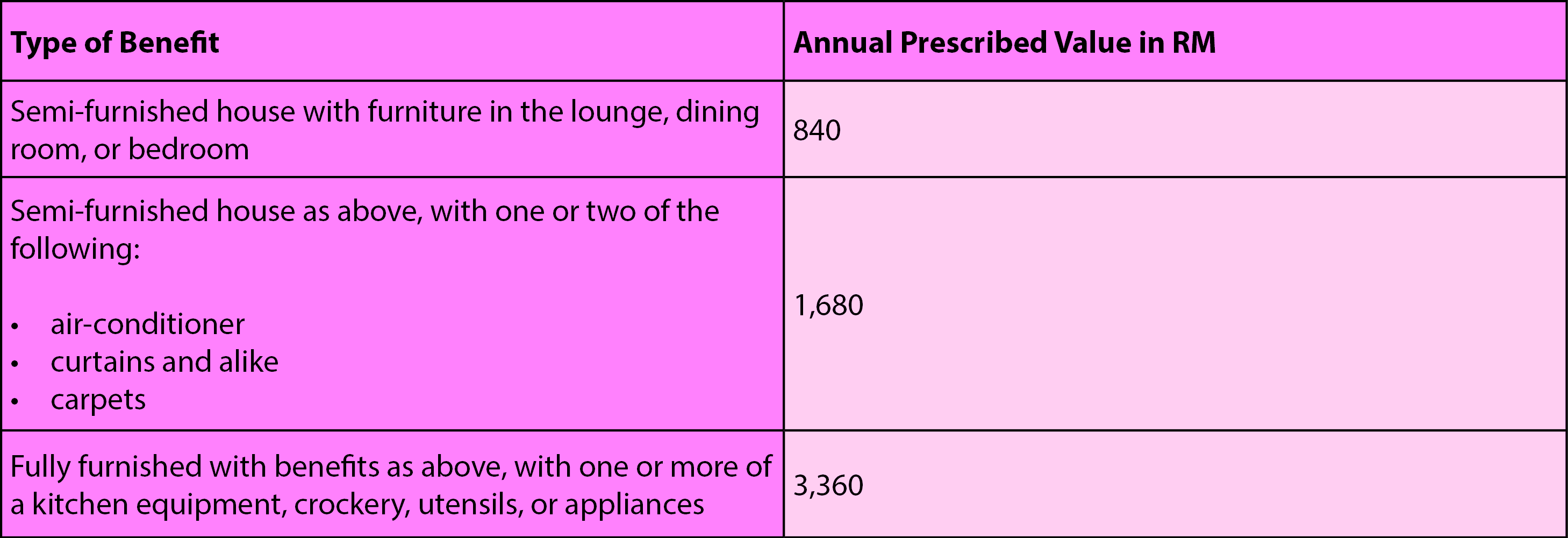

Prescribed Value of Household Furnishings, Apparatus, and Appliances

For a fuller list of prescribed value for benefits in kind, you can check out this official document provided by the Inland Revenue Board of Malaysia.

After calculating your chargeable income from your perks, benefits, and subtracting your tax exemptions and reliefs, you’ve come to your total chargeable income. Which isn’t yet the amount you have to pay, since we haven’t factored in the tax rebates yet!

Tax rebates (or also known as “tax refunds” but done automatically rather than actually refunded to you). Another type of tax rebate, but which is only applicable for Muslim citizens, is the zakat / fitrah. Zakat is a compulsory payment for charity and considered to be compulsory as it is one of the five pillars in Islam. It can be calculated via the Muslim taxpayer’s acquired wealth or income.

| Tax Rebate | Year of Assessment 2009 onwards (RM) |

|---|---|

| Self where chargeable income does not exceed RM35,000 | 400 |

| Separate Assessment for Wife or Husband where the other partner has no total income | 400 |

| Zakat / Fitrah | Limited to total tax charged |

Don’t Forget

The 2016 tax assessment year follows the calendar year, so it is effective from 1st January 2016 to 31st December 2016.

- For individuals without business source, the due date is on or before 30th April.

- For individuals with business source, the due date is on or before 30th June.

- For a non-resident individuals without business source, the due date is on or before 30th April.

- For non-resident individuals with business source, the due date is on or before 30th June.

If you have any other questions regarding personal income tax for the 2016 assessment year, feel free to drop them in the comments section down below!

![]()

About THE AUTHOR

RinggitPlus

Most Viewed Articles

Most Viewed Articles

Tax

Petrol Price Malaysia Live Updates (RON95, RON97 & Diesel)

We provide weekly updates on every Friday at 5pm on the prices of RON95, RON97 and Diesel in Malaysia and a chart that shows the movement of fuel prices across a 6-week period. Bookmark this page now!

Tax

EPF Declares 6.15% Dividend For 2025

The Employees Provident Fund has declared a dividend rate of 6.15% for both Simpanan Konvensional and Simpanan Shariah […]

Tax

KTM Berhad Raises ETS Ticket Discount To 30%

KTM Berhad has upgraded its Electric Train Service (ETS) ticket discount from 20% to 30%, applying the revised […]

Tax

2026 Malaysian Banks Ang Pow Designs: Galloping Into Another Totally Subjective Review

Just when we thought we had finally recovered from year-end feasting and festive chaos, Chinese New Year 2026 […]

Comments (0)