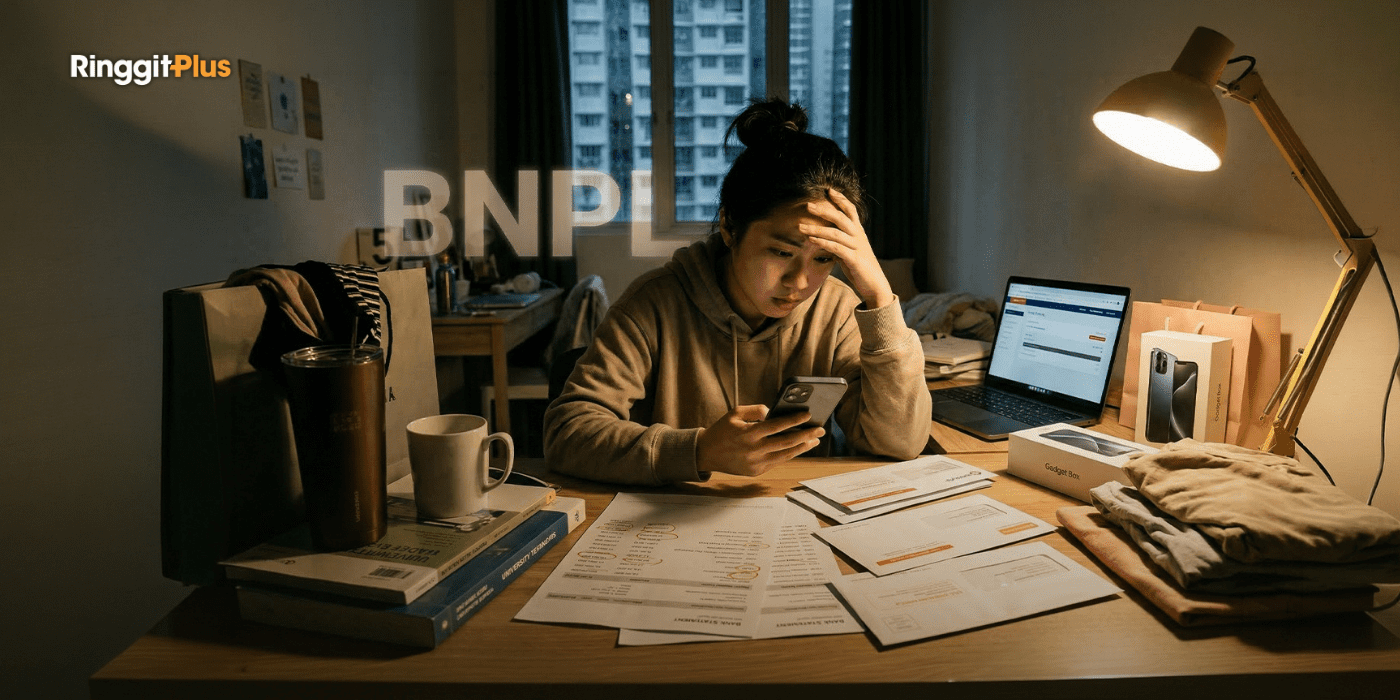

If a large part of your salary is already gone soon after payday, the warning from MCA Youth may sound familiar. Rising living costs, together with easy access to credit cards, personal loans, and Buy Now, Pay Later, or BNPL, schemes, are making it easier for debt to build up among young Malaysians before they have had the chance to build savings.

MCA Youth deputy chairman Mike Chong said many young adults are now using a significant share of their income to repay debt, leaving less room for financial security. The concern is not only about large loans, but also about everyday spending habits that can slowly turn into long term repayment pressure.

Easy Credit Can Mask The Real Cost

Borrowing has become much easier for young adults entering the workforce, especially when payment options are built into online shopping and daily spending. Credit cards, personal loans, and BNPL plans can feel manageable at first because they reduce the immediate pressure to pay in full.

The risk is that once several repayments begin to overlap, a meaningful part of your salary can disappear before essentials, savings, or other priorities are covered. That is one reason this issue is getting more attention. On 12 March, Deputy Finance Minister Liew Chin Tong said about 40% of BNPL transactions in Malaysia are made by youths, pointing to how widely these services are already being used for day to day spending.

Small Purchases Can Add Up Faster Than Expected

A debt problem does not always begin with one major purchase. More often, it builds through repeated smaller spending that feels harmless in the moment, such as food delivery, online shopping, sale items, and lifestyle purchases.

Chong said one of the most useful habits for young workers is tracking monthly spending. A simple record of income and expenses can make it easier to see where money is going, especially when small transactions start adding up more quickly than expected. Without that visibility, it becomes much harder to tell whether your spending still matches what you earn.

Needs Should Stay Ahead Of Wants

The pressure becomes harder to manage when non essential spending starts taking priority over basic needs. Rent, food, transport, and utilities usually have to come first, yet impulse purchases can still take up a large share of income when spending is not planned properly.

This is especially true during online sales or when purchases are split into instalments. A small payment may look affordable on its own, but several small commitments at once can become a much heavier burden over time. The danger is not always one expensive decision, but a string of smaller ones that quietly build into a larger repayment problem.

Borrowing For Daily Spending Can Become A Trap

Chong also cautioned against relying too heavily on credit facilities for regular living expenses. While credit cards and BNPL services can offer short term convenience, they become much riskier when they are used to cover everyday costs that should ideally be paid from current income.

Once that pattern starts, each new month can begin with repayments from the previous one. That reduces cash flow, limits room for savings, and makes it harder to absorb unexpected costs without borrowing again. Over time, this can turn short term convenience into a cycle that is difficult to break.

Emergency Savings And Early Support Still Make A Difference

Building an emergency fund remains one of the clearest ways to reduce reliance on debt. Financial planners often recommend setting aside three to six months of living expenses, but even smaller and more consistent savings can still help create a buffer when unexpected costs appear.

Chong also said financial guidance and counselling can help before the situation becomes more serious. Getting support early may make it easier to restructure debt, improve repayment planning, and regain control before missed payments or rising balances begin to limit the available options.

Financial Habits Need To Start Earlier

The warning also points to a bigger gap in financial education. Chong said stronger financial literacy should be built through schools, universities, and community programmes, so that young Malaysians enter adulthood with a better understanding of budgeting, saving, and responsible borrowing.

Cost Of Living Pressure Can Make Bad Habits More Expensive

For young workers, this issue is becoming more relevant at a time when everyday costs are already rising. When more income is needed for essentials, there is less margin for mistakes, and the impact of repeated borrowing can show up much faster.

That is what makes debt harder to ignore. It does not only affect what you owe each month, but also what you are unable to build, whether that is savings, emergency reserves, or longer term financial stability.

Follow us on our official WhatsApp channel for the latest money tips and updates.

Samuel writes about personal finance and financial news, focusing on how banking updates, policies, and promotions affect everyday money decisions. He enjoys making complicated financial topics easier to follow. Outside of writing, he spends his time watching TV shows and occasionally convincing himself he will only watch one episode.

00votes

Article Rating

SHARE

About THE AUTHOR

Samuel Chua

Samuel Chua

Samuel writes about personal finance and financial news, focusing on how banking updates, policies, and promotions affect everyday money decisions. He enjoys making complicated financial topics easier to follow. Outside of writing, he spends his time watching TV shows and occasionally convincing himself he will only watch one episode.

We provide weekly updates on every Friday at 5pm on the prices of RON95, RON97 and Diesel in Malaysia and a chart that shows the movement of fuel prices across a 6-week period. Bookmark this page now!

Subscribe to our exclusive weekly newsletter and we’ll bring you the week’s highlights of financial news, expert tips, guides, and the latest credit card and e-wallet deals.

Thank you for subscribing!

Stay tuned for what’s to come next in the personal finance world

Comments (0)