Alex Cheong Pui Yin

Previously covered recruitment-related stories and had a short stint as a copywriter for the property industry. She subsequently developed an interest in investment and robo-advisors.

31st March 2022 - 6 min read

With the Employees Provident Fund (EPF) set to open applications for another withdrawal facility on 1 April 2022, EPF members will once more be allowed to take out up to RM10,000 from their EPF savings. This is in hopes that it will provide some financial relief those who are still struggling from the aftermath of the Covid-19 pandemic.

Here are some key details of the special withdrawal facility that you should know before applying for it, based on the FAQ that has been released by the EPF.

Members who are aged below 55 years old are allowed to apply for the facility, including non-citizens and permanent residents. You are also required to have at least RM150 in your EPF savings during the time of application.

The FAQ clarified that members who have applied for previous Covid-related withdrawal facilities are also allowed to make another withdrawal via this latest facility, provided they have the required minimum amount in their EPF savings. Members of the civil service, too, may apply if they are in need of funds, but they risk using government shares that will need to be reimbursed at a later date.

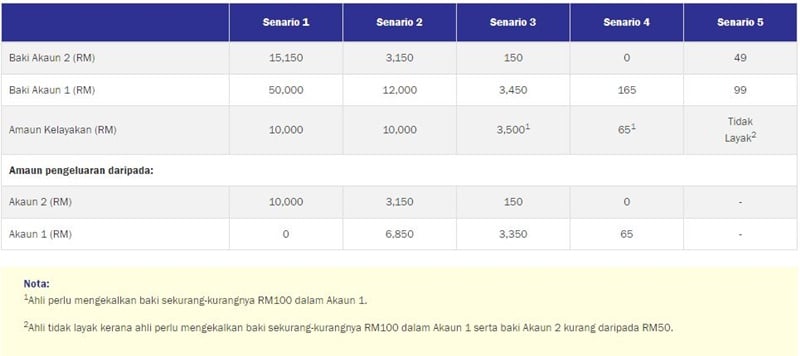

Each member can withdraw between a minimum of RM50 to a maximum of RM10,000, depending on the amount that is available in your EPF savings. You are also required to maintain a minium balance of RM100 in your Akaun 1 after the withdrawal, in order to keep your status as an EPF member.

Note that the funds applied through the special withdrawal facility will be taken from your Akaun 2 first. If the amount in your Akaun 2 is insufficient, then you can access your Akaun 1 savings to top up the remaining amount required. Meanwhile, savings from Akaun Emas (for employees between the age of 55 to 60) cannot be withdrawn under the special withdrawal facility.

Here are several scenarios provided by the EPF to illustrate how the procedure works:

Applications are set to take place between 1 to 30 April 2022.

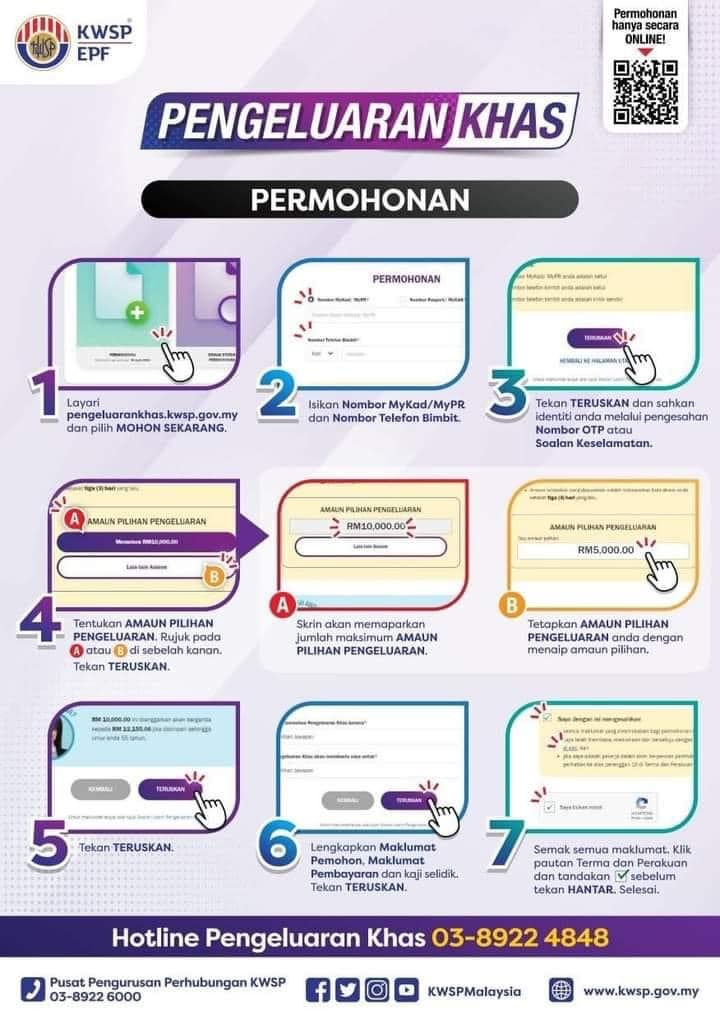

Applications can only be done online via the Pengeluaran Khas portal, which can also be accessed directly from the i-Akaun mobile app. Alternatively, scan the following code to access the portal:

The EPF has also shared a detailed flowchart to guide those who wish to make an application:

Make sure to check on various key details prior to making your application for a smoother process. Also, take care not to be deceived by scammers, who may attempt to present themselves as third parties assisting the EPF in the application process.

The funds will be disbursed starting from 20 April 2022, via one single payment to be credited into your current or savings account. To ensure that you receive your funds without any hitches, make sure that your bank account is still active, and is registered under your name; joint accounts or company accounts are not accepted.

Meanwhile, members who do not have bank accounts due to specific reasons – such as being ineligible to open a bank account, or are bankrupt – can request to collect their special withdrawal funds via standing instruction (Arahan Bayaran). The EPF cautions, however, that those who opt for this disbursement method may not receive their funds as quickly.

If you do collect your funds via standing instruction, you’ll need to wait for the EPF to contact you for collection, after which you can head over to any RHB Bank branches to cash it in.

As for those who do not have a bank account but are eligible to open one, you’re required to do so, and then resubmit your application for the special withdrawal facility.

Members are not allowed to cancel their applications after submitting it, and they are also not allowed to amend the withdrawal amount.

Yes, you are required to replenish the full amount that has been withdrawn, along with an additional 20% of the amount. So for instance, if you decide to withdraw the maximum amount of RM10,000 from your EPF savings this time round, you’ll need to replenish a total of RM12,000 (RM10,000 + RM2,000) in the future.

Just like i-Sinar, 100% of your future contributions will be credited into Akaun 1 until the required amount is fully replenished. Once that’s done, your contributions will revert to the original distribution of 70% for Akaun 1 and 30% for Akaun 2.

The EPF explained that it is to ensure that members will have sufficient savings to live on upon reaching retirement. The percentage was determined based the estimated amount of dividend that a member may lose out on due to the withdrawal, calculated at the average of 5% annual dividend. This is because members are expected to take between four to six years to fully replenish the withdrawn amount (5% x 4 years = 20%).

Applicants can check their application status starting from 9 April 2022, either through the Pengeluaran Khas portal (Semak Status Permohonan), or their i-Akaun (Pengeluaran > Sejarah Pengeluaran).

***

This special withdrawal facility is the fourth of such aids to be provided by the EPF, with the first few being i-Lestari, i-Sinar, and i-Citra. As the government has reiterated numerous times, it is intended specifically for those who are still facing dire financial difficulties due to the Covid-19 pandemic, despite the country being on its road to recovery. As such, Muslim members should be aware that unless they are withdrawing these funds for essential reasons (hajah asliyah) – such as for survival or to repay immediate debts – they will be required to pay a 2.5% zakat.

Finally, if you have any enquiries regarding the special withdrawal facility, you can head on over to the official EPF website, or reach out via the chat system ELYA. Alternatively, contact the EPF via any of their social media accounts, or call the dedicated hotline for this facility at 03-8922 4848.

Previously covered recruitment-related stories and had a short stint as a copywriter for the property industry. She subsequently developed an interest in investment and robo-advisors.

Subscribe to our exclusive weekly newsletter and we’ll bring you the week’s highlights of financial news, expert tips, guides, and the latest credit card and e-wallet deals.

Stay tuned for what’s to come next in the personal finance world

Comments (3)

Thank you

Hi, regarding the replenishment of funds withdrawn, in cases where the withdrawal comes solely from Account 2, am I right to assume the “replenishment” does not apply (including the 20% on top of the amount withdrew) since nothing was taken from Account 1?

bro, read carefully. it says any withdrawal (i.e. whether from Account 1 or Account 2) will be covered by future contribution with additional 20% i.e. 1.2 x the amount withdrawn and this total 1.2x will be deposited in Account 1 to force save by member. so balance after 1.2 x met will then revert back to 70%-30% as before. if you take out rm10000 now, future contribution amounting to rm12000 will be put into Account 1 first. any balance thereafter will be split 70%-30%