How To Choose The Best Personal Loan

Jacie Tan

28th October 2020 - 6 min read

When it comes to applying for personal loans in Malaysia, you definitely have a wide range to choose from. About 70% of personal financing offered by banks in Malaysia fall under Islamic banking too, so there’s no shortage of Syariah-compliant personal financing plans that you can apply for as well. But with so many choices, how do you determine the “good” ones to apply for?

Whether it’s for an emergency or to pay for a planned expense, be aware of the important factors when choosing which personal loan to get.

Know How Personal Loan Interest Rates Work

Most, if not all banks in Malaysia charge flat interest rates for their personal loans – unlike home loans, which charge a reducing loan balance rate. A flat interest rate is a type of interest that is charged on the principal loan amount throughout the tenure of the loan, regardless of the outstanding balance. This means that your effective interest rate will likely be higher than the percentage of interest rate advertised. For example, if you take out a loan of RM10,000 at an interest rate of 8% over 5 years, the total amount of interest you would pay is RM4,000, which is actually 40% of your loan amount.

Therefore, don’t blindly chase after the one with the lowest interest rate. Yes, personal loans with lower interest rates are more attractive, but that’s not the only deciding factor for whether or not a loan is right for you. For example, lower interest rates might come together with a shorter loan term, larger minimum amounts, or higher requirements that you might not be able to meet – which we’ll look at below.

Choose The Right Loan Tenure

In Malaysia, a personal loan tenure can last from 1 year up to 10 years. Choosing the right loan tenure is important because it directly affects your ability to pay it off. The instalments for a personal loan are smaller when your loan tenure is longer, which is why many people opt for longer loan periods. Some also choose to select the longer tenures thinking that they can just pay off their loans early if they wish to later on. On the other hand, some people are overconfident and choose shorter loan periods only to find themselves unable to meet the due payments down the line.

If you do have the ability to pay off your personal loan ahead of schedule, there’s nothing wrong with doing so. However, be aware that most lenders use the Rule of 78 when it comes to calculate loan interest charges. Basically, it means that the borrower is required to pay a greater portion of the interest owed in the earlier part of their loan tenure, thus decreasing the potential savings in paying off the loan early.

On top of that, you could also incur fees for early payment – so try to choose the right loan tenure at the beginning and you will probably be better off.

Be Aware Of All The Fees And Charges

Personal loans come with a few fees and charges, some of which you may not be aware of. They’re not necessarily all bad, but you should still be aware of them so that none of them take you by surprise. For example, you can expect to pay a stamp duty of 0.5% of the whole amount on your personal loan, although there are a few banks that may absorb it. One fee that you shouldn’t be paying for is the processing fee on your personal loan, as banks are no longer allowed to charge for those anymore.

As we mentioned above, some banks also charge you a fee for early termination of your loan agreement. So, if you decide to pay your loan off early, there is a chance that you can be charged a percentage of the remaining amount. This amount is usually a fixed amount or a percentage of the outstanding amount (whichever is higher). Meanwhile, it’s normal to face a penalty fee of about 1% of the current outstanding amount for making late payments.

Lastly, some personal loans may even require you to apply for an insurance policy together with your loan. Known as a Reducing Term Assurance (RTA) or Reducing Term Takaful (RTT) for Islamic financing, this policy is meant to give your loan financial protection in the event of death or total permanent disability, so that you won’t need to burden your family with your loan should anything happen to you. However, it could have the impact of increasing your loan amount by several per cent, so make sure to take this into account if your personal loan requires it.

Don’t Underestimate The Requirements

Different personal loans have different requirements, whether it’s your minimum annual income, age, nationality, employment status, or employment sector. Apply for a personal loan where you pass most of the requirements to get a better chance of being approved.

For instance, civil servants will have a better chance getting their application for a personal loan that is specifically for government employees. And if the personal loan sets “salaried employee” as a requirement, full-time business owners are probably better off applying for a different personal loan.

Of course, don’t forget that your credit score comes into play here too. You may fulfil all the requirements for a personal loan perfectly but still get rejected due to your poor credit rating – so make sure that you have a healthy record of prompt payments in your recent history before applying for a personal loan.

Lastly, banks may be hesitant to offer you a personal loan when you’ve already been rejected by another – so make your choice wisely and apply for a personal loan where you have a higher chance of being approved.

Be A Responsible Borrower

A personal loan can be a useful tool if you use it for the right reasons. It can help you consolidate your debt, ease up your cash flow, and can really come in handy in times of emergency. Borrowers are not required to disclose the reason behind their personal loans to the banks, but that doesn’t mean you shouldn’t think long and hard about why you’re taking out a personal loan. Make sure that it’s a justified decision that you can financially sustain in the long term, and then you can start looking around for the right personal loan for you.

Fortunately, you have some solid and dependable choices when it comes to personal loans on the market, such as the RHB Easy-Pinjaman Ekspres and Citibank Personal Loan, which both offer instant approvals as one of their core features. If you are looking for financing to help with your debt consolidation, then the Standard Chartered CashOne Debt Consolidation Plan or Alliance Bank CashFirst Personal Loan could well be the options you are searching for. For more information on personal loans all in one place, don’t forget to visit the RinggitPlus website.

About THE AUTHOR

Jacie Tan

Most Viewed Articles

Most Viewed Articles

Personal Loans

Malaysia Bank Moratorium: Why You Should Opt For The 6-Month Deferment For ALL Loans (Updated)

EDITOR’S NOTE: This article refers to the 2020 loan moratorium, and the information here may be outdated. Please […]

Personal Loans

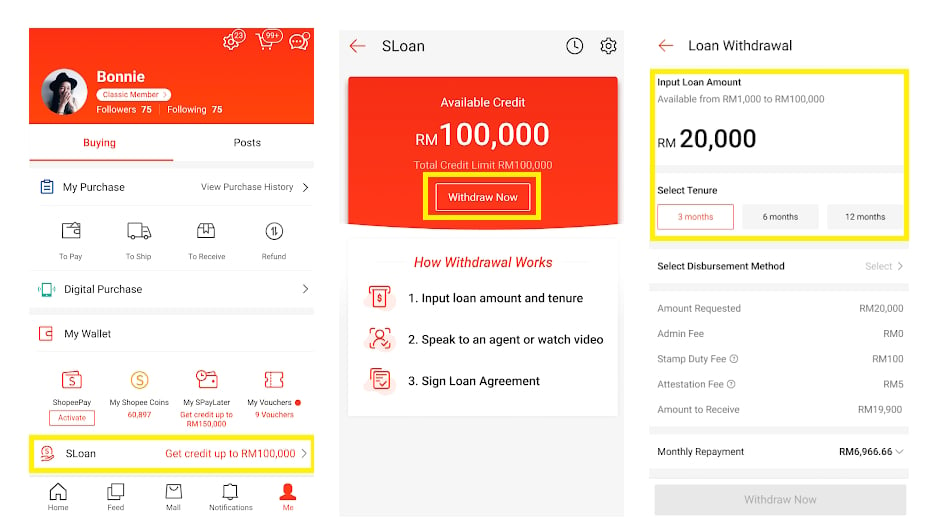

Shopee Rolls Out Personal Loan Service, SLoan

Shopee has expanded its digital financial offerings to now include a personal loan service, dubbed SLoan. At present, […]

Personal Loans

What Do Banks Really Look For In Your Loan Application?

Need a loan? Then you might be curious about what lending banks are concerned with when considering your application.

Personal Loans

Malaysia Loan Moratorium 2021 Guide: Should You Take The 6-Month Deferment For Your Loans?

Under the PEMULIH stimulus package, Malaysia will once again see a 6-month moratorium for all loans, applicable to […]

Related articles

Comments (0)