Latest Articles

The Experts Corner

What To Do When Your Landlord Won’t Return Your Deposit

Not getting your rental deposit back can be frustrating, especially when your landlord has stopped responding or is […]

Business Loans

Selangor Micro-Financing Approval Now Takes 48 Hours

Small business owners in Selangor can now get micro-financing of RM10,000 and below approved in under 48 hours […]

Insurance

Free Health Screenings Available At Allianz Health Festival On 1 August

You can get a free basic health screening and a cancer risk factor assessment this Saturday, 1 August, […]

Bank News

Maybank Adds QR Payments To Samsung Wallet

Samsung Malaysia and Maybank have launched Malaysia’s first Samsung Wallet QR payment feature, letting eligible Samsung Galaxy users […]

Education & Career

Simpan SSPN Plus Adds Zurich Takaful As Fourth Operator

Parents saving through Simpan SSPN Plus now have a fourth takaful operator to choose from, after PTPTN appointed […]

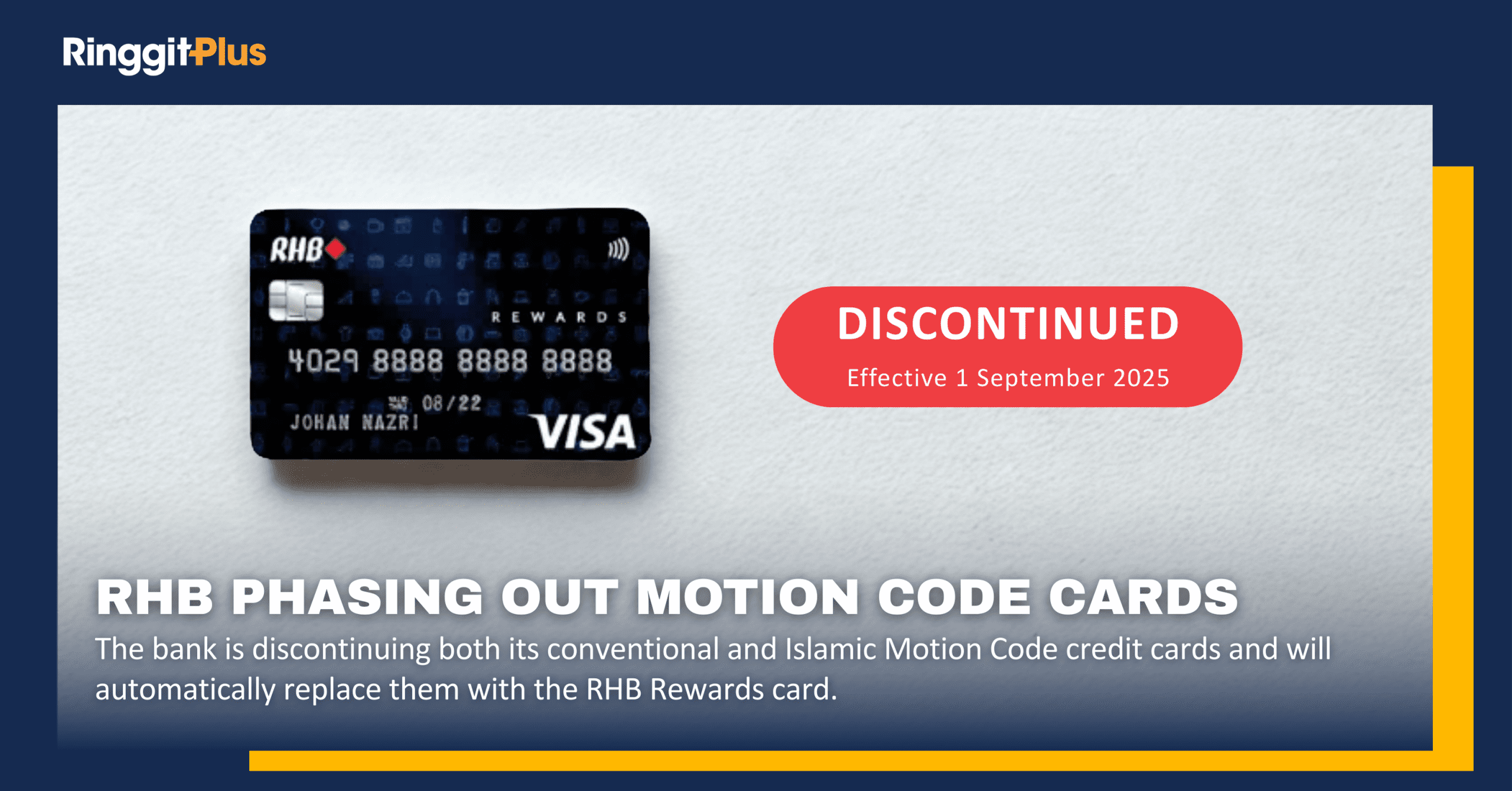

Bank News

RHB Cardholders Get Up To 25% Off Batik Air Fares

RHB Credit Card/-i and Debit Card/-i holders can get discounted fares on eligible Batik Air Malaysia bookings from […]

Personal Finance News

Tourism Malaysia And MYDIN Offer RM5 Million In Travel Prizes

Tourism Malaysia and MYDIN launched the “Jom Jalan MYDIN” campaign, offering more than RM5 million in travel prizes […]

Lifestyle

Selling Second-Hand Items Can Now Support Charity

Selling an old phone or clearing out your wardrobe could now do more than just earn you some […]

Personal Finance News

25,781 Company Jeeps And Pickups Signed Up For Cheaper Diesel

A total of 15,388 businesses covering 25,781 jeeps and pickup trucks have registered under the Sistem Kawalan Diesel […]

Personal Finance News

MR.DIY Club Lets Up To 5 Family Members Share Points

MR D.I.Y. has launched its first loyalty programme, MR.DIY Club, letting up to five family members link their […]

Load More

Most Viewed Articles

Most Viewed Articles

Petrol Price Malaysia Live Updates (RON95, RON97 & Diesel)

We provide weekly updates on every Friday at 5pm on the prices of RON95, RON97 and Diesel in Malaysia and a chart that shows the movement of fuel prices across a 6-week period. Bookmark this page now!

Best Fixed Deposit Promotions and Board Rates In Malaysia

We provide monthly updates on the best fixed deposit promotions in Malaysia with tables showing the top 5 board rates for the duration of 1, 3, 6, 9, and 12 months.

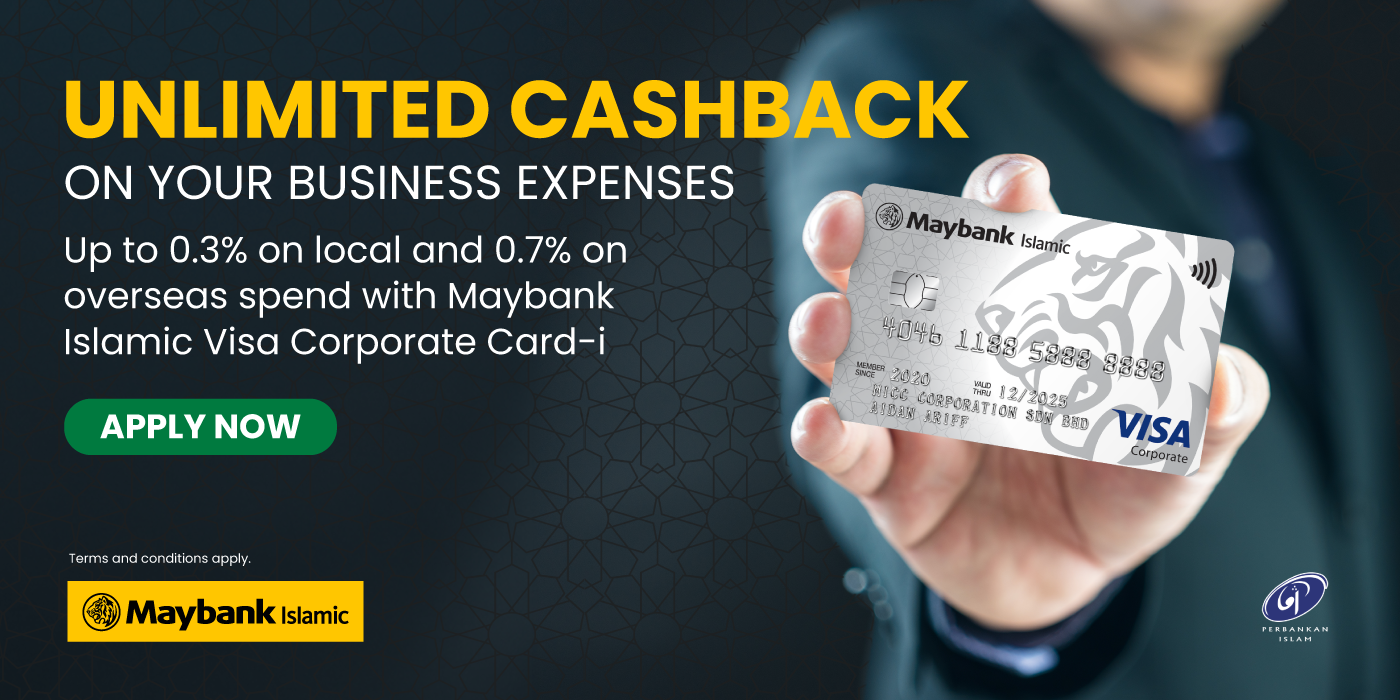

The Corporate Card That Earns Unlimited Cashback On Every Business Spend

By the time month-end comes around, piecing together what the business actually spent across personal cards, reimbursement claims, […]

KAF Investment Funds Berhad Launches Global Islamic Equity Fund

KAF Investment Funds Berhad (KIFB) has launched a new unit trust fund that gives investors Shariah-compliant access to […]

Credit Card Reviews

The Experts Corner

The ringgitplus show

Most viewed articles

The Experts Corner

Petrol Price Malaysia Live Updates (RON95, RON97 & Diesel)

We provide weekly updates on every Friday at 5pm on the prices of RON95, RON97 and Diesel in Malaysia and a chart that shows the movement of fuel prices across a 6-week period. Bookmark this page now!

The Experts Corner

Best Fixed Deposit Promotions and Board Rates In Malaysia

We provide monthly updates on the best fixed deposit promotions in Malaysia with tables showing the top 5 board rates for the duration of 1, 3, 6, 9, and 12 months.

The Experts Corner

Things You Didn’t Know Can Help Reduce Your Credit Card Payment

We’ve got a few ideas up our sleeves to help you bring down that bill and possibly even make future payments much more affordable!

The Experts Corner

Best High Interest Savings Accounts In Malaysia (April 2024)

Make your money work for you by depositing them into the best high-interest savings accounts in Malaysia!